Fraud in UK Financial Organizations

Introduction

Background

Fraud is a practical problem faced by the financial organization in the UK. There is no doubt that fraud is a fundamental and increasing problem in the UK. The overall extent of the problem is hard to quantify. The yearly cost of fraud to UK organizations ranges between £106 billion and £140 billion. According to UK Finance report, in the year 2019, about £1.2 billion was lost due to fraud. Although the influences of these frauds have been far-reaching, internal organizational procedures leave much to be anticipated. According to the study of Pymnts (2019), only 32% of UK organizations have implemented stricter control in their position to deal with frauds, finance dissertation help. As much as 17% have not any procedure in place at all for managing fraud.

Fraud is a pointless expense as organizations can prevent most of it by implementing proper strategies. Certainty fraud management should form a portion of the organization’s overall risk management approach that should, in reality, be an extensive level of duty. From an organizational viewpoint, fraud can be either internal or external in nature. If the business associates and customers are linked with the administrative system, they should be observed as insiders. The majority of internal frauds are prohibited or noticed through internal controls or reviews and signals from customers, employees, and informers. On the other hand, external frauds necessitate diverse strategy, which is subject to prevention.

Fraud prevention presently represents one of the most significant issues in financial organizations (Capgimini, 2015). Typical organizations lose 5% of revenues due to fraud every year, where banking and financial services are the most common victims of such problems (Capgimini, 2015). In sum, possible global fraud-based losses are above $3.5 trillion. In the year 2014, losses on remote banking fraud in the UK has increased to £35.9 million, representing a 59% growth than in 2013. Online banking fraud comprises £29.3 million in 2014 in the UK, representing a 71% increase than in 2013. The total worth of fraudulent transactions undertaken by utilizing cards is about €1.33 billion in 2012, signifying 14.8% growth than in 2011 (Capgimini, 2015). Fraud has reached to epidemic level in the UK and requires observation as a critical safety issue. It is a crime to which the people in the UK are most probably to face losses. Its influence on private segments has resulted in the instability of individual organizations. 85% of reported fraud in the years 2019 and 2020 was cyber empowered. Apart from that, there is also the prevalence of transaction fraud and accounting fraud among organizations in the UK. The consequences of fraud are extensive, which requires banks and financial organizations to become more proactive regarding managing fraud. Financial organizations need to demonstrate that they can measure and manage risk by implementing active strategies that give proven advantages. It is vital for organizations to apply and maintain comprehensive fraud prevention approaches (JDSupra, 2021).

Fraud damages the financial performance of organizations, and they are forced to minimize the cost to income ratios. It also results in loss of reputation, which is hard to repair and leads to customer loss and market shares. Fraud also comprises fines from regulators, and the expenditures are related to investigations and possible prosecution by legal procedures. Therefore, proper strategies must be used by organizations to deal with this problem (Okoye & et al., 2019).

Dig deeper into Uk Retail Oligopoly with our selection of articles.

When it arrives at fraud management, the majority of financial organizations face problems like different transaction structures, piecemeal fraud detection solutions, and high operational expenditures (Okoye & et al., 2019). In specific fraud fields, shortcomings in financial organization’s strategy to fraud controls interpret them to non-obedience with regulations and possibly lead to losses. There is also a challenge of balancing customers’ experience and expectations with added safety. Customers typically pursue quicker and more superficial processing of transactions. However, in fraudulent prevention solutions, financial organizations apply increased safety steps, which is in direct conflict with customers’ experience. An efficient fraud strategy is crucial for financial organizations. Unable to bring proper fraudulent management system can bring monetary, reputational, and punitive risks. On the other hand, a fraud management strategy can also provide competitive benefits by enhanced customers’ confidence and better customer experience (CICM, 2019). Appropriate fraud solutions can provide significant advantages within the business, reducing the expenses and threats, enhancing customer satisfaction, and empowering innovation.

Aim and Objectives

The key aim of the research is to understand fraud in financial organizations and the management methods that can be used for controlling it. Based on the research background, the key objectives of the research will be:

To understand the fraud problem faced by financial organizations

To understand the reason people involve in fraud

To understand the strategies for managing fraud problem in financial organizations

To know how fraud strategies can impact the performance and survival of financial organizations

Literature Review

Frauds in Organizations

Fraud comprises unlawful, corrupt, and misleading functions conducted either by an organization or an individual performing according to their capability as an employee of the organization. Fraud arrangements are frequently highly complex and hence hard to recognize. It often requires months for specialists to unravel fraud in an organization (CFI, 2020). In accordance with Agwor (2017), fraud is any kind of dishonesty conducted to trick others to their harm or the disadvantage of others or incur a loss for others. In contrast, the committers have a clear understanding of his/her thoughtful lie, dishonesty, or benefit over the acquitted and unwary target. According to Gary & et al. (2011), fraud includes dishonesty, distortion of facts, and suppression of material truths in order to obtain a specific one-sided benefit over others. Fraud is considered to happen when an individual or group of individuals with complete knowledge or important details distorts such truths to obtain something of value, for example, money or assets. Association of Certified Fraud Examiners (1999) additionally describes fraud as the utilization of one’s job for individual development by the thoughtful exploitation, abuse, or utilization of organizational resources or assets.

In financial organizations, fraud occurs whenever an individual knowingly performs or intend to perform a scheme or pretense in order to deceive or to obtain any of the sums of money or assets possessed by or within the protection or control of the organization by way of dishonest or deceitful pretenses, depictions or promises. Odi (2013) acknowledges that fraud in financial organizations shakes the basis and credibility of the organizations, resulting in considerable financial losses. The constant growth in cyber scams has adversely minimized customers’ faith in the organization's capability to safeguard their assets, deposits, or funds. Due to fraud, customers or depositors in financial organizations are conscious regarding the security of their funds and financial information. They expect that the organizations find a solution so that fraudulent activities are reduced.

Fraud is a common organizational issue, and no country is free from it. Fraudulent event is witnessed across the country, which continues to betray every good intention and effort made by organizations and people towards economic development. In the year 2019, fraud cases in the UK were worth £1 billion, where chances of internal frauds doubled in values in 2019 in comparison with previous years. More than £192 million of alleged fraud against organizations involves traditional misappropriation against businesses, manipulation of accounts, and abuse of job position. Technology-empowered frauds have continued to increase fraud cases. Fraud cases against the public in the UK were worth £40 million in 2018 (Waligora, 2020). This requires an extensive fraud management system to apply in financial organizations.

Fraud Theory

White-Collar Crime Theory: The word crime is initially linked to a crime that happens on streets, comprising crimes like physical violence. Nevertheless, fraud is a crime, which is structured crime conducted by specialists, where the preys are general people, who are conscious that they are sufferers of this crime. This crime is linked with financial and business functions, commonly termed as white-collar crime. According to Sutherland (1940), there are three aspects of white-collar criminals. The first is that white-collar criminals are typically professionals. The second is that as the perpetrators are professionals, the law applied to them are not too heavy. Third is that recognition of criminals and sufferers is much problematic as the majority of individuals do not simply observe the crime. This theory states that as fraudsters find themselves effective at their crimes, they start to obtain particular secondary enjoyment in the knowledge that they are tricking the world, that they are demonstrating their supremacy to others. People conducting fraud require having strong self-esteem and great confidence that they will not be sensed. The typical personality types comprise someone determined to obtain success at any rate, self-absorbed, self-confident, and frequently egotistical (Abdullah & Mansor, 2015).

Fraud Triangle Theory: According to Cressey (1950), three aspects inspire fraud, which are pressure, rationalization, and opportunity.

The pressure in a company is one of the triggers that inspire fraud. Pressure in this context mentions the financial stress, for example, lifestyle, debt crisis, and reliance on drugs, among others. The luxury lifestyle is considered to make someone keep abreast of the latest trends in terms of fashion, culinary and automotive, among others. The characteristic of a luxurious lifestyle is not only owned by individuals who are in an economic group and does not rule out the likelihood of having a lavish lifestyle. The demand to keep up-to-date with the latest styles, without being followed by the growth of income, can compel someone to commit fraud to fulfill the desire (Ardi & et al., 2019).

Moreover, rationalization is a vital component in fraud. Fraud committers always intend to justify their activities. Perpetrators require creating specific morally good thoughts before involving in unethical activities. Rationalization mentions to explanation and excuses that unethical conduct is different from criminal function. The third aspect of fraud triangle theory recommended is opportunity. Poor inner control in a company, a low level of supervision, and abuse of authority can trigger prospects for a person to commit fraud. Within the three aspects in fraud triangle theory, the opportunity aspect is the most likely aspect that is required to be reduced through strengthening internal control and initial identification of fraud attempts (Ardi & et al., 2019). Based on fraud triangle theory, when financial stress arises, followed by opportunity, i.e., felt that the act would not be noticed. The rationalization that the show does not disrupt can make an individual expert commit fraud. This theory is the foundation of the creation of fraud theories.

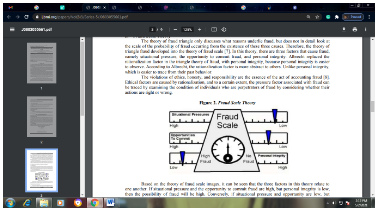

Fraud Scale Theory: Fraud triangle theory only discusses the causes of underlying fraud but does not observe at the scale of the possibility of fraud happening from the presence of three reasons. Hence, the theory of fraud scale is developed. According to this theory, there are three aspects that cause fraud, which are situational stress, the prospect to commit fraud, and personal honesty. Albrecht (1984) replaced the rationalization aspect in the triangle theory with personal integrity, as it is simpler to observe. The rationalization aspect is much abstract, unlike personal integrity, is simpler to trace from historical behavior. Infringement of ethics, morality, and duty are the core of the function of fraud. Ethical aspects are generated by rationalization, and to a certain level, the stress aspect related to fraud, which can be traced by evaluating the condition of people who are committers of fraud by considering whether their activities are right or wrong.

On the basis of the above picture, it can be observed that three aspects of fraud are associated with each other. In case the situational stress and prospect to commit fraud are high. However, personal honesty is low; the likelihood of fraud will be increased. Contrariwise, if the situational anxiety and opportunities are intense, but emotional honesty is high, then the possibility of fraud is common.

Fraud Diamond Theory: In fraud diamond theory, a component named capability is added to three initial fraud elements. Wolfe & Hermanson (2004) claimed that although perceived stress might coexist with opportunity and rationalization, it is improbable for fraud to occur until the fourth component, i.e., the ability is also present. In short, the possible committer requires possessing the capabilities to commit fraud. Wolfe & Hermanson (2004) stated that opportunity opens the entrance to top fraud and incentive, i.e., stress and rationalization result in an individual towards the door. Nevertheless, capability empowers the individual to identify the open entrance as a prospect and to take benefit of it by walking through constantly.

In the above model, capability refers to possessing the essential behaviors or skills and qualifications for the individual to commit fraud. It is where the fraudster identified specific fraud prospects and the power to turn copy into realism. Position, intellect, personality, coercion, dishonesty, and stress are supporting components of ability. Mackevicius & Giriunas (2013) stated that not every individual who has motivation, prospects, and realization can commit fraud owing to a low level of capability to carry out or to hide it. Albrecht & et al. (1984) opine that this component is of specific significance when it concerns a large scale and long run fraud. Moreover, Albrecht & et al. (1984) consider that only the individual who has exceptionally high capacity will be capable of understanding the existing inner control to recognize its weaknesses and to utilize them in planning fraud. In a similar context, Wilson (2004) reveals that rationalization and ability are interconnected, and the strength of every component impacts others.

The initial aspect of empowering fraudsters to possess the ability to commit fraud is the position holding in the organization. Wolfe & Hermanson (2004) stated that work and role by an employee could perfect his way to breaking organizational faith. Fraudster comprehends and able to exploit inner control weaknesses and utilizing the class, function or authorized access to the most significant benefit. Intelligent, experienced, and creative individuals with a solid grasp of controls and weaknesses undertake most of the present day’s biggest frauds. This knowledge is utilized to impact a person’s concern for authorizing access to the system. Fraudsters have strong self-esteem and great confidence that they will not be detected and believe that they can merely take themselves out of trouble. Such confidence and arrogance can impact involvement in the fraud. The more confident the individual becomes, the lower the forecasted expense of fraud will be.

New Fraud Triangle Model: Another essential theory of fraud is the new fraud triangle model. This theory comprises features of financial and non-financial causes. Kassem & Higson (2012) categorize the aspects that generate copy, dissimilar from fraud triangle theory. Based on revising specific previous works on fraud, Kassem & Higson (2012) stated that fared derives from individual, occupational and external stress. These stresses can occur due to financial and non-financial pressures. In a similar manner, work stress can also happen to owe to financial and non-financial aspects. Therefore, Kassem & Higson (2012) prompted external auditors that the focus or motive for committing fraud can be personal, work, or external pressure. Every kind of stress can also happen to owe to financial and non-financial aspects. Kassem & Higson (2012) also argues that every fraud theory is an extension of fraud triangle theory and requires to be incorporated with one framework, which is additionally termed as a new fraud triangle framework. It comprises inspiration, prospect, integrity, and capability.

This theory clarifies that the commencement of the development of the theory of fraud started with the idea of white-collar crime. This theory comprises con as a class of misconducts undertaken by elite people. Therefore, white-collar crime theory is essentially less specific to discuss fraud activities as they are many generals. Hence, the idea of the fraud triangle seems to re-concentrate the discussion on fraud functions. This theory is more concentrated on fraud in comparison with white-collar crime theory. This is because the fraud triangle theory explains the reasons for the copy. It gives three aspects that inspire fraud, which are stress, rationalization, and prospect.

Research Design and Methodology

Research Philosophy

There are three types of philosophies that help to understand reality in research, which are positivism, interpretivism, and realism. This particular research is based on interpretivism philosophy. Throughout the investigation, it is believed that the subject fraud problem in financial organizations and its strategies is subjective. The subject should be observed from an individual viewpoint, and therefore the researcher's personal opinion plays a vital part in the research. The research is based on understanding the meaning of fraud and various strategies which can impact organizational performance. It is considered that the reality about the fraud problem is socially created, and therefore by reviewing works from multiple authors can help to know the truth about the subject. The fraud problem in organizations can be comprehended by shared meaning and generating consciousness about the issue. This research is not only based on facts and figures but on interpreting and understanding the importance that humans attach to their activities. Therefore, to understand the actions of fraud, there is a need to move beyond facts and figures and understands the behavioral aspects that make people for conducting fraudulent acts and the strategies that require to be taken for preventing such actions.

Research Approach

There are three approaches, which can be used for conducting any research, qualitative, quantitative, and mixed. In this research, the qualitative approach will be used. The reason for choosing this approach is because the subject is subjective, and there is no possibility for conducting any statistical analysis between variables. By using a qualitative approach, the issue is analyzed through narration and description. In this research, only qualitative data is used. Qualitative research helps to address the objectives through personal narratives and studying the subject from a subjective viewpoint. Since the research subject is more about understanding the concepts of fraud and fraudulent activities and strategies to mitigate them, opinions of people regarding fraud in financial organizations and how it influences the performance and experiences of people on fraud strategies on survival of organizations, qualitative approach is suitable. Understanding the behaviors of people who commit fraud requires observing the subject from a subjective viewpoint. Hence, a qualitative approach is used as it will help to fulfill the research objectives.

Research Design

Research design gives the outline and plan, which can be utilized for gathering and evaluating information. There are three kinds of research designs that can be used in research, which are experimental design, descriptive design, and causal design. In this research, an experimental design will be used. In experimental design, the key focus will be to obtain thoughts and insights regarding the subject. It is conducted in order to give a better understanding of a situation. In this context, this research is also performed to obtain insight regarding fraud problems in financial organizations. There are various kinds of experimental research designs, which are literature search, depth interview, focus group, and case analysis. In this research literature, the search method is used. The literature search is one of the fastest and inexpensive methods to understanding the subject. Every research starts with a literature search. There is an incredible amount of data accessible in online libraries, which is will be used for conducting the research.

Research Types

There are two types of reasoning that can be used in research which are inductive and deductive. In this research, inductive reasoning will be used. The qualitative approach mostly follows inductive reasoning. This research will begin with observation of theories and concepts regarding fraud, fraudulent activities, and fraud management strategies through literature search. This will help to develop the basis for conducting the research and will help to understand the key theoretical concepts underlying the subject.

Data Collection and Analysis

Based on sources, there are two types of data that can be used in research, which are primary and secondary. In this research, only secondary data has been used. Online journals, articles, books, and websites will be used as secondary sources in order to conduct the literature. In order to analyze the data, the grounded theory method will be used. It is a systematic strategy used for the qualitative approach. In this method, the theory will be developed by collecting qualitative data. It involves the utilization of inductive reasoning. In this method, data will be reviewed thoroughly, and on the basis of the review, concepts regarding the subject will be identified, and theory will be made.

Presentation of Findings and Conclusion

Fraud Management System

The fraud management system mentions the procedures and frameworks utilized in order to recognize an organization’s exposure to fraud threats and to apply controls, processes, and training to avert, notice and react to critical fraud-oriented threats. Fraud management activities can hence be extensively categorized into a preventive, detective, and reactive fraud management activities. Preventive fraud management functions are those activities, which are intended to minimize fraud and wrongdoing from happening initially. Such actions comprise undertaking fraud threat evaluation, creation of robust inner mechanisms, code of conduct, associated standards, due diligence, proper communication and training, the introduction of strategies and procedures, and corporate governance (Ohando, 2015). Preventive controls intend to reduce intention, limit the opportunity for possible offenders to vindicate their activity. Fraud prevention is the duty of every person in the organization. Okoye & et al. (2019) reported that fraud management in organizations holds, in its extensive sense, the consciousness of many elements of fraud, for example, human component, organizational behavior, and awareness of likelihood and consequences of fraud, among others. Fraud management is based on the controls and strategies developed by organizations for minimizing the threat of fraud and losses by better fraud control activities. Fraud management requires to be approached methodically. The basic process begins from the prevention of fraudulent acts as it is better than the exposure of fraud. Since fraud detention activities unable to stop every possible committer, organizations require to certify that systems are in the position that will point incidences of fraud in a timely way. This is accomplished by fraud recognition. Fraud recognition strategy should comprise analytical and other processes to indicate anomalies and the introduction of reporting instruments that provide for communication of alleged fraudulent activities. Essential components of a comprehensive fraud recognition system should comprise exception reporting, data mining, trend evaluation, and constant threat evaluation.

Fraud recognition can point to continuing frauds that are occurring or wrongdoings that have already happened. Such arrangements may not be influenced by the development of prevention methods. Even if wrongdoers are caught up in the future, recovery of losses will only be achieved by fraud identification. Fraud recognition permits the development of inner systems and controls. Various frauds take advantage of the deficits in the control structures. By recognition of such copies, management can be tightened, making it challenging for possible culprits to commit fraud (Ijeoma & Aronu, 2013).

According to Omokaro & Ikpere (2019), reactive fraud management activities intend to take counteractive measures and fixing the damage generated by fraud. In every occurrence, management requires to evaluate the adequacy of the existing internal control atmosphere, specifically those controls, which have a direct impact on the fraud act, to consider the requirement for developments. Internal inspection can specifically support an organization to control fraud by delivering guidance on the threat of fraud, directing on design or competence of internal controls to reduce the danger of fraud happening, and by supporting management to enhance fraud deterrence and observation strategies. An efficient inner review plan requires comprising an assessment of fraud controls intended to address the considerable fraud threats faced by an organization.

Fraud Management Strategies

Fraud prevention and fraud recognition have vital roles to play, and it is improbable that either will ultimately prosper without others. Hence, it is essential that organizations consider both fraud prevention and fraud recognition in developing an effective strategy to deal with fraud. The following diagram demonstrates the elements of fraud management strategies that can be used by organizations to stop fraud.

There are several components of efficient fraud management strategy and are closely connected with each other. Fraud recognition strategy functions as a warning by sending a message to likely fraudsters that the organization is vigorously dealing with fraud and that processes are in place to recognize any unlawful functions that have happened. The likelihood of being caught frequently encourages a possible committer to avoid fraudulent acts.

Fraud risk training and consciousness: each time a major fraudulent incident occurs, individuals who were innocently close to the fraud are surprised that they were unconscious of what was happening. Hence, it is vital to increase consciousness through official education and training programs. It should be a portion of the fraud management strategy. Specific consideration requires to be paid to those employees, supervisors, and managers who are functioning in high threat fields and also to those who have a responsibility in prevention and recognition of fraud (CIMA, 2008).

Reporting method: Creating proper reporting methods is one of the critical components of fraud management. Many fraudulent activities are known or doubted by individuals who are not involved in those activities. It is a challenge for an organization to inspire those individuals to disclose such actions as it is for their benefit.

Development of rigorous ethical culture: Attitudes within an organization frequently lay the basis for a high and low fraud atmosphere. When slight immoral activities are overlooked, more enormous frauds undertaken by the top level of management can also be treated in a similarly compassionate manner. In such an atmosphere, there can be a threat of total failure of the organization either by a sole disastrous fraud or by the collective burden of various more minor cons (CIMA, 2008).

Comprehensive internal control system: Overall duties for internal organizational control require being at the highest level in the organization. Within the Companies Act, directors are liable for maintaining proper accounting records. The combined code recommends that the board in an organization require maintaining a comprehensive system of internal control in order to protect the investment, fund, and assets. This should comprise processes developed to reduce the threat of fraud. The board requires ensuring that the inner organizational system is efficient (CIMA, 2008).

Integrated fraud management functions: To efficiently deal with fraud, contemporary financial organizations continuously updated the management structures with new regulations, statistical frameworks, and obtained knowledge. This procedure becomes more straightforward and much effective with centralized systems.

Utilizing real-time external information: Various financial organizations are no longer satisfied with merely using regular transactional details to deal with fraud and also seek external information gathered from third-party suppliers and intelligence from social networking websites in order to enhance the capabilities of fraud recognition (Graydon Report, 2019).

Advanced technology solutions: Customers in the present day’s desire simple and easy to utilize financial services. Financial organizations which are capable of safeguarding their transactions, money, and assets through using advanced technology like advanced authentication by mobile technology, can generate competitive benefit and can enhance the performance through satisfying customers’ expectations (Graydon Report, 2019).

Fraud Management and its Impact on Performance

The loss of fraud in financial industries like banks, insurance, credit card and other financial organizations is staggering. The successful fraud strategies give the assurance of considerably reduced loss on fraud and its impact on performance. According to Ijeoma & Aronu (2013), adoption of holistic method to fraud management not only assist financial organizations in preventing fraud, but also effectively balance the functions within and among fraud management lifecycle. Effective application of fraud management lifecycle enhances the possibility of practical fraud threat management and hence survival of financial organizations. According to the study conducted by Ohando (2015), on connection between fraud management and financial performance of banks, it can be observed that there is positive connection between fraud management practices and financial performance. It was also discovered that preventive and detective fraud management activities have strong positive connection on financial performance. Githecha (2014) in his study demonstrated that fraud detection technology implementation has strong positive connection with financial performance in banks. Apart from that, strong governance and regulation are also positively connected with the financial performance of banks. Kuria & Moronge (2013) in their research stated that technology and governance when implemented as control instrument greatly determine the growth of financial organizations. The outcomes of their research also demonstrated that regulating the financial industry can result in the growth of the industry through minimization of fraudulent activities. The study of KPMG and EY states that organizations that utilize companywide fraud awareness training reduce the fraud losses by about 52%. Their research additionally indicates that financial organizations are putting more time and resources to reducing fraud, with the emphasis typically on fraud recognition and reporting. The efficient implementation of fraud management strategies is elucidated by financial disciplines within organizations. Every area of financial organization, i.e. from accounting to customer service is better able to understand the requirements and value given by fraud management.

Conclusion

The effect of fraud management on financial organizations cannot be overstated, particularly with the pervasiveness of fraud occurrences in modern times. On the basis of the report it can be stated that fraud management influences organizational performance and survival. Every financial organization is victim of fraud occurrences and that the utilization of preventive and detective fraud management functions enhances the performance of organizations. Therefore, it is recommended that regulation and supervision in financial organizations must be stricter, so as to minimize fraud occurrence. This will keep management of financial organizations on alert and control measures will be put on position to stop and to discourage fraud. Financial organizations also require inspiring practices like fraud threat evaluation, robust inner control, surprise external audit, board oversight and antifraud strategy. Reactive fraud control functions, for example communication to employees that the administration taken appropriate measures, loss recovery and sanctions should be done regularly for enhancing operational effectiveness of financial organizations.

References

Abdullah, R. & Mansor, N., 2015. Fraud Triangle Theory and Fraud Diamond Theory. Understanding the Convergent and Divergent For Future Research. International Journal of Academic Research in Accounting, Finance and Management Sciences, Vol. 5, No. 4, pp. 38-45.

Agwor, T. C., 2017. Fraud Prevention and Business Performance in Quoted Manufacturing Companies in Nigeria. European Journal of Accounting Auditing and Finance Research, Vol. 15, No. 9, pp. 71-80.

Ardi, R. D. A. & et. Al., 2019. Development of the Theory of Fraud Towards the New Fraud Triangle. International Journal of Business and Management Invention, Vol. 8, No. 3, pp. 56-61.

Albrecht, S., 1984. Deterring fraud: the internal auditor’s perspective. Institute of Internal Auditors Research Foundation, pp.1-42.

Association of Certified Fraud Examiners, 1999. Report to the Nation on Occupational Fraud. [Online] available at: https://acfe.com/documents/2010R [Accessed 30 March 2021].

Capgimini, 2015. Fraud Solution for Financial Services. [Online] available at: https://www.capgemini.com/in-en/wp-content/uploads/sites/6/2017/07/fraud_management_in_banking_brochure.pdf [Accessed 29 March 2021].

CFI, 2020. Corporate Fraud. [Online] available at: https://corporatefinanceinstitute.com/resources/knowledge/finance/corporate-fraud/ [Accessed 30 March 2021].

CICM, 2019. External Business Fraud in the UK. [Online] available at: https://www.cicm.com/wp-content/uploads/2019/10/External-Fraud-report_FINAL.pdf [Accessed 29 March 2021].

CIMA, 2008. Fraud risk management A guide to good practice. [Online] available at: https://www.cimaglobal.com/Documents/ImportedDocuments/cid_techguide_fraud_risk_management_feb09.pdf.pdf [Accessed 30 March 2021].

Cressey, D. R., 1950. Other People’s Money. Patterson Smith.

Gary, P. & et. Al., 2011. Fraud: A review and research agenda. Accounting business and public interest, pp. 138-178.

Githecha, D. K., 2014. The effect of fraud risk management on the financial performance of commercial banks in Kenya. University of Nairobi.

Graydon Report, 2019. External Business Fraud in the UK. [Online] available at: https://www.cicm.com/wp-content/uploads/2019/10/External-Fraud-report_FINAL.pdf [Accessed 30 March 2021].

Ijeoma, N. & Aronu, C. O., 2013. The Impact of Fraud Management on Organizational Survival in Nigeria. American Journal of Economics, Vol. 3, No. 6, pp. 268-272.

JDSupra, 2021. With Fraud Against UK Businesses at Epidemic Levels, Businesses Need to Know How to Protect Themselves. [Online] available at: https://www.jdsupra.com/legalnews/with-fraud-against-uk-businesses-at-7098742/ [Accessed 29 March 2021].

Kassem, R. & Higson, A., 2012. The New Fraud Triangle Model. Journal of Emerging Trends in Economics and Management Sciences.

Kuria & Moronge, 2013. Effect of fraud management practices on the growth of insurance companies in Kenya. International Journal of Innovative Social & Science Education Research, Vol. 2, No. 1, pp. 26-39.

Mackevicius, J. & Giriunas, L., 2013. Transformational Research of the Fraud Triangle. ISSN Ekonomica, Vol. 92, No. 4, pp. 150-163.

Odi, N., 2013. Implication of fraud on commercial banks performance in Nigeria. International Journal of Business and Management, Vol. 8, No. 15, pp. 144-150.

Ohando, R. O., 2015. Relationship between fraud risk management practices and financial performance of commercial banks in Kenya. University of Nairobi.

Okoye, E. I. & et. al., 2019. Fraud Risk Management and Corporate Performance of Deposit Money Banks (DMBs) in Nigeria. Journal of Accounting and Financial Management, Vol. 5, No. 4, pp. 33-46.

Omokaro, B. E. & Ikpere, O. C., 2019. The Impact of Fraud Management Activities on Organization Survival in Nigeria. International Journal of Research and Innovation in Applied Science, Vol. 4, No. 4, pp. 20-27.

Pymnts, 2019. UK Study: Businesses See Fraudsters As ‘Ahead Of Industry’. [Online] available at: https://www.pymnts.com/news/b2b-payments/2019/vocalink-uk-business-fraud-accounting-scam/ [Accessed 29 March 2021].

Sutherland, E. H., 1940. White-Collar Criminality. American Sociological Review, Vol. 5.

Waligora, R., 2020. Alleged fraud for 2019 has reached over £1 billion. [Online] available at: https://home.kpmg/uk/en/home/insights/2019/12/alleged-fraud-for-2019-has-reached-over-1-billion-pound.html [Accessed 30 March 2021].

Wolfe, D. T. & Hermanson, D., 2004. The Fraud Diamond: Considering the Four Elements of Fraud. The CPA Journal.

Dig deeper into Financial Sector Practice with our selection of articles.

- 24/7 Customer Support

- 100% Customer Satisfaction

- No Privacy Violation

- Quick Services

- Subject Experts