Corporate Social Responsibility and Its Impact on Sustainability

- 14 Pages

- Published On: 30-10-2023

Introduction

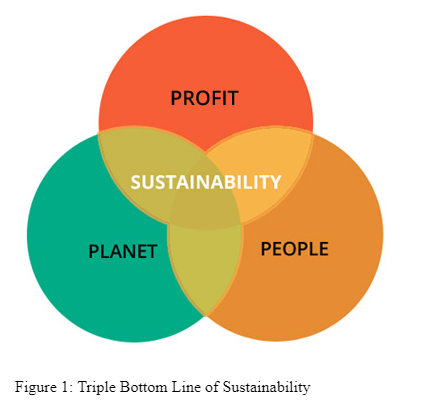

Corporate Social Responsibility remains to be a widely discussed topic within academic, business, legal, environmental, and societal discourses owing to its evolving nature and impact. From the review of various pieces of literature, it can be extrapolated that Corporate Social Responsibility was resultant of the sustainability concept, which brought forth a renewed emphasis on the impact of business organisations whilst they are pursuing their economic goals (Eskerod and Huemann, 2013). This emphasis aimed at promoting sustainable practices whereby organisations are required to put into consideration the ability of future generations to meet their needs in equal proportions as they are currently utilizing resources to meet their current needs. Students pursuing environmental studies dissertation help often explore how CSR initiatives add value to sustainable development goals. In essence, the sustainability concept requires private institutions, public institutions, and citizens to safeguard the environmental and promote societal conditions whilst pursuing current economic goals/needs (Caradonna, 2014). The concept of sustainability was expounded or explained further through the concept of triple bottom line of sustainability whereby organisations are deemed to be sustainable when they aim at achieving a perfect balance between economic, environmental and societal objectives as illustrated in the image below.

If not deduced, it is inferred from various definitions of corporate social responsibility (CSR) that it is an act merely aimed at enabling organisations to achieve the triple bottom line of sustainability. This is to say; through CSR an organisation is able to achieve a perfect balance between its economic, environmental, and societal objectives/goals. In the writings by Yang & Guo (2014), they stated that the International Organisation for Standardisation described CSR as the activities undertaken by an organisation to ensure it positively impact on the environment and society as enshrined under ethical practices, the law, and both national and international norms. As for the World Bank, it described CSR as the commitment of organisations to undertake sustainable economic development by working towards improving the lives of their employee and their extended families as well as the society in a manner that is good for the organisation and for development. On its part, the International Labor Organisation described CSR as the voluntary initiative undertaken which is beyond its legal obligations. In essence, CSR is considered a complement rather than a substitute for social policy or governmental regulation. The image below illustrates the concept of CSR This present discourse aims at providing an in-depth discussion on the concept of CSR whilst incorporating various case studies to demonstrate proper understanding. The discussion will commence with a look at the components of CSR, followed by the triple bottom line of CSR, thirdly, the increased importance of CSR. The penultimate section will state the benefits of CSR and thereafter conclude by highlighting the future perspective on CSR.

Components of Corporate Social Responsibility

Considering there is no single universally agreed definition of CSR, it equally means its components are expanded to fit with different definitions. One of the key components of CSR is environmental protection and based on this component, CSR initiatives are expected to ensure that when the organisation (private, public, and individual citizen) is undertaking processes that will result in revenue generation, the environment and in particular, natural resources should be protected from depletion i.e. used in a sustainable manner. Secondly, the organisation should ensure the products and services that have been produced do not negatively impair the environment. For example, they should have low carbon emissions as well as low resultant waste and they should be efficient in terms of energy consumption (Schüz, 2012). By undertaking environmental protection, a business organisation ensures that as it achieves it economic goal itis also scoring on the triple bottom line of sustainability in regards to protection of the environment. The second component of CSR is community involvement where a business organisation, government agency, and private citizens undertake actions that surpass the impact of their monetary donations. Such involvements include spending time with members of the community and engage in people development activities, volunteering to community work, and sharing of knowledge with the intent of improving the livelihood of community members (Popa & Salanta, 2014).

The sixth component of CSR is ethical practices in the marketplace and in particular on activities such as product manufacturing, selling practices, disclosure, packaging, and labeling, pricing, advertising and marketing, and distribution. In each of these activities, companies are expected to apply ethics as part of CSR by addressing issues such as product safety and environmental impact, marketing to children, privacy and proper use of technology (Aras et al, 2010). The seventh component of CSR is health promotion whereby business organisations are expected within their role to promote the health and well-being of its employees and the society. This normally leads to the creation of a healthy working environment and safeguarding of health determinants within the society such as quality of water and air. In addition, it is also within the mandate of CSR for business organisations dealing with food stuff to ensure their products and services do not pose any danger to the health of consumers nor does it promote unhealthy eating habits (Kujala et al 2013). The fifth component of CSR is upholding of business standards in regards to ethical practices, fair and accurate financial representation, and labor standards. Such standards are usually set at the organisational, industry, national, and/ or international level. Morrison & Bridwell (2011) wrote that the increased level of globalisation has bolstered the adoption of international standards such as those prescribed by the International Standards Organsiations and the International Financial Reporting Standards.

Dig deeper into Motivation and Team Building at Apple with our selection of articles.

Lastly, sustainability can only be guaranteed by the assurance of the existence of qualified or skilled labour in the future to equally utilize the available resources in a sustainable manner. Ergo, CSR must consist of education and leadership development through contributions that are aimed at improving the quality of education that is availed to the society (Thiel, 2015).Toyota Motor Corporation stands out among many for its continued efforts to implement CSR initiatives within its organisational culture and operations. In 1992, it developed a policy document titled the ‘Earth Charter' through which it stipulated its strategy on environmental protection in regards to vehicle exhaust emissions and the overall impact of its manufacturing process on the environment. One of the strategies that was developed is the continued development of technology that enables its processes and products to be cleaner and efficient thus gaining an additional competitive advantage. Moreover, the charter makes the provision for each affiliate, subsidiary or branch location to undertake its unique CSR activities that are pertinent in addressing local needs. Summarily, Toyota’s CSR practices revolve around the component of environmental protection, education and leadership development. Examples of Toyota’s CSR initiatives include the Toyota Volunteer Centre where employees partake in community development activities, scholarship of students in Kenya through the Toyota Kenya Foundation, student exchange programmer in Vietnam, the Toyota Teach (an educational programme in South Africa) that is spearheaded by the Toyota South Africa Foundation (Tanimoto, 2014).

The Triple Bottom Line of Corporate Social Responsibility

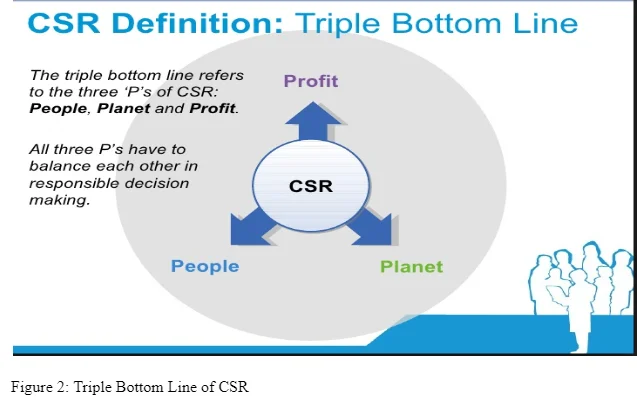

As earlier mentioned the concept of CSR is derived from the concept of sustainability, and as it has been demonstrated through the listed components it basically aligned towards achieving an economic goal that is in equal measures to the environmental and societal goal. Ergo, whilst companies are under the pressure of generating maximum returns on investors’ capital they are equally expected to add value towards the organisational impact on the environment and society at large. This is referred to as the triple bottom line of CSR, whereby the economic bottom line emphasizes on the attainment of financial success whilst putting into consideration the strategy should safeguard the sustainability of the organisational as well as the human capital. As an addition to this point, Egels-Zandén & Wahlqvist (2007) stated that CSR is concerned with how a business organisation generates its revenue rather than how it spends. As such CSR activities ensure revenue generation process abides by ethical standards, legal requirements, and both national and international norms. Under the environmental bottom line, CSR concerns itself with the impact of organisation’s operations, products and services as well as the levels of emissions and waste, and how these are handled to ensure there is no negative impact on the environment. Through the social bottom line, an organisation undertakes CSR activities that address issues pertaining to labor security, wages, working environment, gender and ethnic diversity as well as overall contribution to community development. The concept of triple bottom line of CSR is illustrated in the image below (Esmaeilpour & Barjoei, 2016).

The triple bottom line of CSR has necessitated the emergence of a new area of knowledge known as social and environmental reporting through which organisations develop a well-structured report highlighting on how they addressed or attained their CSR's triple bottom line. Much of current literature/discourses focus more on the auditing aspect of social and environmental reports rather than the actual reporting. Social and environmental auditing of organisations has emerged as a new area of knowledge under CSR, where auditors undertake verifications tests to assess the actual impact of an organisation on the environment and the society. This new area of knowledge demonstrates the emphasis placed on the triple bottom line of CSR (Sharma & Khanna, 2014).

The Increased importance of Corporate Social Responsibility

To this extent, this discourse has demonstrated through substantive evidence the importance of CSR both at the organisational level, environmental level, and societal level. This section will use various themes to further explain the increased importance of CSR. Based on the writings by Shafer (2015), it is noted that CSR has gained increased importance because of globalisation which requires organisations to achieve consistent business practices as displayed by international players or organisations in other countries, otherwise local businesses will be deemed unfit to engage in international trade or they will be perceived as non-evolved considering their failure to keep up with the trend. New technology such as social media has increased the importance of CSR since organisations' activities are now exposed to the public who can form either positive or negative opinion about organisations much to its advantage or disadvantage. Moreover, new technology is redefining the importance of CSR since technological companies are still expected to partake in CSR activities whilst their operations usually have less impact on the environment but a massive impact on the society. Lastly, new technology has enabled global information sharing within few minutes, an aggressive media, and keen stakeholders, which collectively has increased the likelihood of discovery of organisations that are not undertaking CSR activities and this will have a resultant effect of negative news coverage subsequently leading to erosion of organisational value, bad reputation and diminished brand image (Md & Akinnusi, 2012).

Unprecedented risks place increased importance on CSR since in the turn of an event an organisation can be portrayed to the World as unethical due to non-compliance of CSR principles as enshrined under the different components. For example, with the implementation of new labor laws reducing working hours, organisations that previously subjected their employees to longer working hours in contradiction to the legally allowed hours will be susceptible to the risk of legal liabilities once the new law is enacted (Valentine & Fleischman, 2008). Additionally, increased importance of CSR is also attributed to the fact that there is a greater cost or liability for misconduct arising from unethical practices, violation of legal requirements, and contravening of national and international norms (Harazin & Kósi, 2013).

The case example of Nike in 1998, best demonstrate the increased importance of CSR. The manufacture during that year recorded a decline in its financial performance of which it attributed this to brand rejection by customers owing to media report that its employees working at its factories were being mistreated (Nisen, 2013). In 2001, Pfizer was under fierce criticism from Oxfam and lobby groups in South Africa because of its pricing policies that were labelled as moral bankruptcy since the company was selling its drugs at unfairly higher prices making them unaffordable to millions of people who were ailing (Watson, 2001).

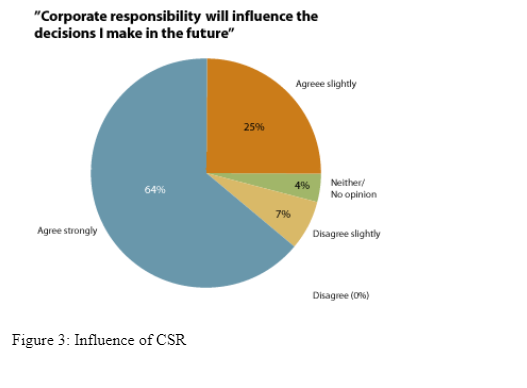

These case examples prove that CSR has gained greater importance to a level whereby organisations have to keep on their triple of CSR or else they would be exposing themselves to unprecedented risks as witnessed by Nike and Pfizer. Moreover, Forte (2013) argued that with increased access to information, consumers are gaining more knowledge and considering there are many options from competitors it means they hold a higher bargaining power; part of the organisational facets they consider before making a purchase decision is their level of CSR. A study conducted by the Burson-Marsteller showed that majority of people will form a perception about an organisation and ultimate a purchase decision based on their CSR activities. This finding is illustrated in the image below (Harazin & Kósi, 2013).

Source: http://www.ecrc.org.eg/uploads/documents/articles_csr%20main%20concepts.pdf

Benefits of Corporate Social Responsibility

Before embarking on the benefits of CSR, Sachs & Maurer (2009) stated that the only obvious demerit of CSR is that it creates an additional operational expense for the organisation that would have otherwise been an additional profit for the organisation; however, he assures that the benefits outweigh the demerit.

In the studies by Chatjuthamard et al 2016, they wrote that CSR accords organisation numerous advantages under sustainable competitiveness and they include the enhancement of the organisation's reputation and brand image, more efficient mode of operations, increased ability to attract and even retain the best employees, increased customer loyalty that results in increased sales and subsequent improved financial performance. As for Forte (2013), he stated those organisations that engage in CSR activities are capable of attracting and retaining quality business partners and investors. Secondly, CSR earns an organisation trust from the community who in turn will cooperate with it to ensure it prospers. Thirdly, CSR enhances the relationship between an organisation and the government, which builds it political capital.

Conclusion

When private and public organisations started to implement sustainable practices they ushered in the era of corporate social responsibility, which required businesses to operate in a manner that will guarantee a balance of economic, environmental, and societal aspects. Though it is considered to be a voluntary act by the organisations, its importance has increased to an extent some components or principles of CSR have been enshrined in the law. Ergo, it can only be envisioned that CSR will continue to be part of organisational culture as well as individual morality and it is bound to increase in its scope owing to its increased importance.

Depending on the industry where a business organisation operates in and even the unique needs of the local area, businesses apply different forms of CSR activities all with the intent of ensuring their economic pursuits are in line with ethical standards, legal requirements, national and international norms. In essence, the different components of CSR ensure that an organisation is able to protect the community it consider as a market for its product and/or services as well as the source of human capital and the environment, which provides it with raw materials and space to conduct its operations. In conclusion, despite CSR contributing to an increased cost of operation, its benefits outweigh this demerit at unrivaled levels as it collectively results in increased profits for the organisation.

References

Aras, G., Aybars, A., & Kutlu, O. (2010). Managing corporate performance. International Journal of Productivity and Performance Management, 59(3), 229-254

Caradonna, J. L. (2014). Sustainability: A history. New York: Oxford University Press

Chatjuthamard, P., Jiraporn, P., Tong, S., & Singh, M. (2016). Managerial talent and corporate social responsibility (CSR): How do talented managers view corporate social responsibility? International Review of Finance, 16(2), 265-276.

Egels-Zandén, N., & Wahlqvist, E. (2007). Post-partnership strategies for defining corporate responsibility: The business social compliance initiative. Journal of Business Ethics, 70(2), 175-189.

Eskerod, P. and Huemann, M. (2013). Sustainable development and project stakeholder management: What standards say. International Journal of Managing Projects in Business, 6(1), 36-50.

Esmaeilpour, M., & Barjoei, S. (2016). The impact of corporate social responsibility and image on brand equity. Global Business and Management Research, 8(3), 55-66.

Forte, A. (2013). Corporate social responsibility in the united states and Europe: How important is it? the future of corporate social responsibility. The International Business & Economics Research Journal (Online), 12(7), 815-819

Harazin, P., & Kósi, K. (2013). Social challenges: Social innovation through social responsibility. Periodica Polytechnica.Social and Management Sciences, 21(1), 27-38.

Huang, C., Yen, S., Liu, C., & Huang, P. (2014). The Relationship Among Corporate Social Responsibility, Service Quality, Corporate Image And Purchase Intention. International Journal of Organizational Innovation (Online), 6(3), 68-84.

Kujala, J., Rehbein, K., Toikka, T., & Enroth, J. (2013). Researching the gap between strategic and operational levels of corporate responsibility. Baltic Journal of Management, 8(2), 142-165.

Linger, H., and Owen, J. (2010) The Project as a Social System: Asia-Pacific Perspectives on Project Management. Australia: Monash University Publishing [Online] retrieved from http://books.publishing.monash.edu/apps/bookworm/view/The+Project+as+a+Social+System%3A+Asia-Pacific+Perspectives+on+Project+Management/171/OEBPS/c11.htm [accessed on 28 January 2017]

Md, H. K., & Akinnusi, D. M. (2012). Corporate social and environmental accounting information reporting practices in swaziland. Social Responsibility Journal, 8(2), 156-173

Morrison, E., & Bridwell, L. (2011). Consumer social responsibility - the true corporate social responsibility. Competition Forum, 9(1), 144-149.

Nisen, M. (2013) How Nike Solved Its Sweatshop Problem. Business Insider. [Online] retrieved from http://www.businessinsider.com/how-nike-solved-its-sweatshop-problem-2013-5 [accessed 28 January 2017]

Popa, M., & Salanta, I. (2014). Corporate social responsibility versus corporate social irresponsibility. Management & Marketing, 9(2), 137-146.

Rouf, M. A. (2011). The corporate social responsibility disclosure: A study of listed companies in bangladesh. Business and Economics Research Journal, 2(3), 19-32.

Sachs, S., & Maurer, M. (2009). Toward dynamic corporate stakeholder responsibility. Journal of Business Ethics, 85, 535-544.

Shafer, W. E. (2015). Ethical climate, social responsibility, and earnings management. Journal of Business Ethics, 126(1), 43-60.

Sharma, J. P., & Khanna, S. (2014). Corporate social responsibility, corporate governance, and sustainability: Synergies and inter-relationships. Indian Journal of Corporate Governance, 7(1), 14-38.

Schüz, M. (2012). Sustainable corporate responsibility - the foundation of successful business in the new millennium. Central European Business Review, 1(2), 7-15.

Tanimoto, K. (2014). Japanese approaches to CSR. Sheffield, U.K: Greenleaf Pub. Ltd.

Thiel, M. (2015). Unlocking the social domain in sustainable development. World Journal of Science, Technology, and Sustainable Development, 12(3), 183-193.

Valentine, S., & Fleischman, G. (2008). Professional ethical standards, corporate social responsibility, and the perceived role of ethics and social responsibility. Journal of Business Ethics, 82(3), 657-666.

Yang, L., & Guo, Z. (2014). Evolution of CSR concept in the west and china. International Review of Management and Business Research, 3(2), 819-826.

Watson, R. (2001) Oxfam Accuses Pfizer of ‘Moral Bankruptcy’ British Medical Journal. 323:186

Continue your journey with our comprehensive guide to Bronfenbrenner's Ecological Systems Theory.

- 24/7 Customer Support

- 100% Customer Satisfaction

- No Privacy Violation

- Quick Services

- Subject Experts