Role of It In Qatar Central Bank

Chapter 1: Introduction

1.1: Background

Exchange of information has become critical to organizations as they graduate from the Industrial Age on to the Information Age, where every piece of information needs to be documented and made readily available, accessible and usable while its correctness and security are ensured. Considering the limitations on the ability of humans to manage data and information at such a level of sanctity, the information technology revolution powered by computers, internet, and social media; supported by the infrastructure necessary for office automation and Management Information Systems (MIS), have taken over the task.

Thus, information technology is expected to help store, manipulate and enable the generation of reports. It has to take up the responsibility to collate, transmit, log and record the data in an intelligent way to facilitate rational decision-making and presentation in a proper form. In this manner technologies have turned into game-changers in improving organizational efficiency and functioning. Further, information technology in terms of networking helps the organization to connect, replicate and transmit data between multiple sites. From a security perspective, IT protects data from external risk and fraud. Thus, the concept of IT in an organization has grown into an influential factor and has become a huge drive affecting organizations performance (Aksoy and DeNardis, 2008).

MFor many years, there have been discussions whether the IT revolution is paying off with regards to improving efficiency. Research in the 1980s could not establish a positive relationship between IT investment and productivity. On the other hand, the introduction of IT was found to bring down the performance of human resources and the phenomenon was named “Productivity Paradox” (Lucas, 1999). However, a decade of studies, at the company as well as country levels, have proved the positive impact of IT investments, as the digital revolution has given humans the ability to manipulate data with mathematical accuracy, to transmit it with high efficiency and to manage it effectively. Additionally, the calculation power available to mankind has seen an exponential increase on the back of the IT revolution (Tansey, 2003). However, the attendant benefits are realized only when such an important weapon is put to particular use in the organizations.

While organizational efficiency is about efficient use of the resources available to the organization; information, human resources, and finances are all regarded as critical assets. Information is an invaluable resource, which groups have tapped into for gaining competitive advantage as well as improving their performance. Information technology offers this edge with regards to information by allowing greater efficiencies in terms of time, cost and resource usage. It further highlights the capabilities that could enable the organization in differentiation and thereby, growing and strengthening their position (Mitchell, 2002). Such efficiency is as much important in the non-profit sector, including the Central Banks, which form the backbone of the financial system of a country.

Central banks deal with the monetary and economic affairs that are relevant to the development of a nation. Though an independent body, the Bank deals with fluctuating currency values and exchange rates. The targets laid out for a Central Bank to drive the development of the nation are tremendous and penalties paid for the inconsistencies are borne by the entire nation (Hasan and Mester, 2008). The credibility of the Bank in laying out policies and driving growth are vital, as it forms the face of the entire financial system of a given country for the outside world. Further, the Bank is expected to behave as the shock-absorber under volatile external environmental conditions such as recession or war or natural disaster. Attaining economic balance with available resources, multiple influencing elements, and fickle circumstances is a Herculean task shouldered by a Central Bank. Unless optimal use of resources or efficiency becomes an internal goal, the crown of the financial system cannot focus on the economic efficiencies of the country. This reiterates the significance of organizational efficiency and performance of the Central Banks (Lohhman, 2003).

This study reflects the case of Qatar Central Bank, which was established in the name of Qatar Monetary Agency (QMA) in 1973, to assume the duties of a Central Bank. Though technology was not a part of the organization then, today, in 2016, QCB has evolved into an organization supported by information technology and the paperless environment (Qatar Central Bank, 2016). This investigation aims at understanding if the use of IT at QCB has led to increased efficiencies in the Bank.

1.2. Significance of the Study

The importance of this study comes from the view that information technology is key to effectiveness and economic development. Progress in IT has no doubt had and continued to have the highest impact on the global economy, making it possible to gather, process, and transfer information at great speed and lower cost. It has thus enabled quality enhancements and efficiency in all types of industries and services around the world. Thus, the major significance of the study is to assess various kinds of technologies that could be used in the banking sector and their impacts could also be understandable.

Banks are becoming increasingly dependent on the Internet and its application to conduct its operations and network those at geographically distant locations. To keep up with the international economy and also the inter-connected world, the Central Bank needs to develop dependable, unified and adaptable systems and employ sound risk management tools in place. As the Bank needs to offer electronic services and online operations, the stress on them to stay technologically sound has become compulsory and crucial. Here, the primary significance is just related to gaining the intellect about the information technology.

While some of the technologies are vital for the day-to-day activities, the others are needed for ensuring a steady performance. Further, the other banks that fall under the mandate of Central Bank have been rendering internet-based financial transactions, cash control and transmission of funds. These activities need to be regulated by the Central Bank to warrant their safety, security and legality while improving the service quality to consumers. Thus, information technology has made in-roads into every aspect of banking and thereby become an essential requirement for the central banks like QCB to lead and guide the financial system (Qatar Central Bank, 2012). However, IT efforts and investments bear no significance unless they enable the Bank to deliver efficiency in performance. At the same juncture, it could be stated that analyzing the working pattern of the central bank could also be treated as the primary significance of the current study. Here lies the importance of the present study.

1.3: Aims and Objectives of the Study

Aim:

The principal aim of the study is to assess the impact of information technology on the working efficiency of central banks. For the same purpose, the case study of Qatar central bank has been taken.

Objective:

- To understand the relationship between IT and performance efficiency in Qatar Central Bank.

- To assess the impact of IT on decision-making effectiveness in banking

- To identify the role of IT in creating the business process quicker and accurate in banking sector

- To recommend various ways to improve performance and efficiency through information technology.

1.4: Focus and Purpose of the Study

The whole focus of the study laid down on the banking industry and the use of information technology by the central bank. Here it is required to understand that the central banks are needed to use such technology which is updated and highly advanced as they need to handle the operations of commercial banks. Thus, the entire focus has been given to the central bank with respect to using the information technology. The purpose of the study is to shed light on the use of IT in the banking industry. Further the transformation into the IT with respect to banking sector has also taken into special consideration. Another purpose of the study is to assess the impact of IT on the performance of central banks. For the same purpose, the various operations and functional activities of the central bank has been studied or investigated articulately.

1.5: Framework Analysis

Here, the proposed research methodology is entirely qualitative in nature. Interpretive research philosophy has been used along with the inductive approach to the study. The subjective information has been used. Further, the interviews have been taken so that the real scenario and usage of IT could be studied. Additionally, both primary and secondary sources of data collection have been used. To analyze the data the thematic analysis has been taken into priority.

1.6: Structure of the Study

This study is divided into the following chapters. A brief description of each section is explained.

1.6.1: Chapter 2 Literature Review

This chapter will present the literature review, which includes the previous studies conducted on the organizational efficiency, significance of IT, the influential factors and the usage of IT in the various processes and systems of Central Banks in general and QCB in particular. This chapter thus establishes the available literature and need for this study.

1.6.2: Chapter 3 Research Methodology

This chapter describes the methodology for conducting the study. It describes the methods used for data collection, sampling, and analysis. In addition to these aspects, the limitations of the study are also defined in this chapter.

1.6.3: Chapter 4 Results

This chapter presents the analysis of the data collected from the sample using survey and interprets the results and findings of the survey. It enables the study to highlight any efficiency that has resulted in the QCB as a result of IT.

1.6.4: Chapter 5 Recommendation and Conclusion

This chapter presents main findings and makes various recommendations based on the knowledge gained from the study. The focus of this chapter would be to make suggestions for the improvement of IT utilization in Qatar Central Bank with regards to its efficiency.

Chapter 2: Literature review

2.1: Introduction

This chapter will present the literature review, which includes the previous studies conducted on the organizational efficiency, significance of IT, the influential factors and the usage of IT in the various processes and systems of Central Banks in general and Qatar Central Bank in particular. This chapter thus establishes the available literature and need for this study. Overall, the in-depth light on the selected subject matter could be spread from this section.

Established in 1993, Qatar Central Bank is authorised by law to issue the national currency and act as the bank for the government and the bank of banks, in addition to its main task of managing the monetary policy of the country. It is paid capital has been raised in line with the development witnessed by the national financial and banking sector.

QCB environment at that time was majorly paper based; there were few simple systems (HTML) for major business only. The reason behind this is a lack of manpower resources and high technology cost at that time. Before implementing the cheque system, banks representatives gather in the central clearing room in Qatar Central Bank to exchange and settle cheque, and before settlement, cheques had to be examined by hand at each stage, which required a large amount of manpower. This entire procedure takes around one day, and cheque settlement takes from one to three days depending on the number of cheques.

QCB found out that technology can facilitate the procedure of cheque exchange, validity and settlement. QCB's role is of supervision and acting as a bank for all banks operating in Qatar; there is no direct connection between each bank. QCB should be intermediate between banks to assure validity and settlement. So the idea of implementing the system invented from here. ECC is an electronic image-based cheque clearing solution. It is undertaken by Qatar Central Bank and is designed to provide end-to-end nationwide clearing of cheque within the same day. ECC provides the means to electronically transfer cheque images and completely replaces the traditional physical routines of moving paper cheque between the banks and clearing houses.

The online cheque compensation system enables QCB to reduce the tedious and time-consuming manual method availing funds at the beneficiary's account within minutes of depositing the cheque and presents faultless management software for the cheque and the whole clearing cycle.

In addition to that, there was no system for the budget, each department has its budget, and the concerned department needs to know how much budget has been consumed from the total allotted budget. So the department assigns an employee to collect invoices of each project by contacting purchase section and takes the update and enter it into excel file and keep the contract of each budget in archive file after the final revision from the legal department.

Technology facilitates the process by implementing the budget system, and each department has access to it, so they know how much budget they have and how much is consumed. Legal Department upload contract after revision with a logical link to each department budget.

To make complete use of information technology, Qatar Central Bank has established an Information Security Committee (ISC) and made it compulsory for all the banks in Qatar to become a member of this committee. Further, the Ministry of Information & Communications Technology, ictQATAR have come up with Qatar National Information Assurance Policy, NIA Policy (equivalent to ISO 27001) for improving the overall Information Security and Technology Controls of the entire Qatar banking industry. Moreover, the Ministry of Interior, MOI supports the banking industry to fight the cyber security criminals through its Cyber Crimes Investigation Centre.

To overcome from the challenges of information loss, Qatar Central Bank has given strict directives to have their own disaster recovery site. In case, if any bank fails to comply with such directives, Qatar Central Bank puts heavy penalties on them. By having disaster recovery site, banks can duplicate the entire IT services at the DR site. Earlier data recovery was just limited to replicating application data to a remote site; however, with the advancement in the technology, banks can duplicate entire IT services at the DR site. Thus, through frequent data replications, banks can keep up with the data and moreover, it automates failover and failback of entire business services such as email.

The definition of information technology states the use of technology or technical infrastructure for the purpose of storing, extracting and disseminating the hefty amount of information. The definition of efficiency in organizational aspects is to perform exceptionally by using all the potential in the desired direction and using the resources in a proper way to achieve the business objectives.

2.2: Information Technology and Performance Efficiency

Various factors contribute to the efficiency improvement of the organizations. Out of all these aspects, the major one is the information technology. Various studies have revealed that there is a direct linkage between the information technology and performance efficiency. Without such aspects, the organizations can never sustain in the world market. The efficiency has simple meaning as it measures or compares the difference between resource input and outputs. The lacking aspects into the outputs as compared to the inputs could be treated as a deficiency. The efficiency through information technology thus is a very natural process.

In the views of Hill and Scudder (2002), integrating IT into businesses increases efficiency and permits companies to build better relationships with the customers and saves cost and time. The findings of Pires and Aisbett (2003) and Reunis et al. (2005) are in line with the views of Hill and Scudder (2002). According to them, IT has enabled the geographically dispersed users to share database and messages instantly with a large number of receivers. Further, use of electronic data interchange (EDI) has changed the way information flows and thus has resulted in better performance efficiencies (Aksoy, Pelin and DeNardis, Laura, 2007).

The advancement in the technological and communication has changed the scenario of business operations. The banking industry just requires aligning with the external technological environment and needs to introduce the technical solutions within the internal environment. It will automatically affect the level of business operations and inherit the efficiency as well. According to various management studies it has been found that the information technology helps in increasing the banking capabilities in various ways. Majorly the process becomes smoother and faster. The banking industry now days have become globalized, so the load or the burden of work is also huge on them. So, information technology enables to make the process faster. Further, with the help of information technology the connectivity of banks with various participants has also improved which is a part of efficiency improvement (Gershenfeld, Neil, 2000).

Other than this, the technology works on particular coding-decoding system which enables to minimize the chance of errors or defaults while implementing the operations. It is to acknowledge that the advanced technology stores the information in well manner and chances of errors are next to impossible. In the case of any error of defaults, it could be rectified with immediate effect. The level of efficiency has surpassed its peak after the introduction of internet banking. The intranet and inter-technology enabled to create own servers which are beneficial in terms of enhancing the efficiency of banking operations. The management studies revealed that the level of efficiency could be measured by the amount of transformations and innovations introduced within the banking industry. Both central and commercial banks have witnessed lots of innovations within the industry and functionality. The role of information and communication technology is immense in ensuring the improving in the organizational process through meeting the expectations of customers and stakeholders at zenith.

2.3: Impact of IT on Commercial Banks

The commercial banks are those banks that deal with both customers and the central bank. The commercial banks act as interlink between the central banks and the customers. They directly establish the platform for the customers where they can deposit, withdraw or save their money and can do their financial activities. It is to acknowledge that the commercial banks need to work according to the needs of their customers (Aksoy, Pelin and DeNardis, Laura, 2007). However, the most important aspect is that the commercial banks work for the best of their country and residents of that country. For the same purpose, the commercial banks implement various strategies that allow them to fulfil both the purposes.

The foremost benefit of implementing IT in banking is that the customers could be connected with any part of the world. The internet banking is one option that has been provided to the customers. Due to the international banking the customers could do their transactions just by sitting in any corner of the world. Every branch is well connected and has access to the central database of a commercial bank. The capacity to store and disseminate the information is so effective that it could be extracted by any branch. Thus, the internet banking has brought a huge revolution in the banking services. Through internet and intranet technologies the branches of commercial banks are interconnected, so it becomes easy to entertain customers at various places. Therefore, the internet banking and intranet have facilitated the customer convenience. It indicates the positive impact at the mindset of customers (Doyle Stephen, 2000). They are satisfie, and their banking operations are also positive.

A study performed by Binuyo and Aregbeshola (2014) found that IT enhances the return on assets and return on capital of the South African Banking industry. They suggested that banks should devise proper policies for maximum utilization of existing IT infrastructure rather than making an additional investment in IT and communication (Binuyo, O Adekunle and Aregbeshola A Rfiu, 2014). Another study conducted by Luka and Frank (2012) shows that IT helps banks in improving their efficiency and effectiveness in service delivery. It enhances their competitive position, managerial decision making, and business processes so that better services can be delivered to the customers (Luka, K Matthew, and Frank, A Ibikunel, 2012).

The commercial banks have extended the utility of technology one step ahead and have done tie-ups with various ventures. Paying bills have become easy as the banks have good connectivity to their accounts and creditors accounts. Credit cards and debit cards are a good example of ensuring the customer convenience. The authors in various studies have revealed that no other industry has witnessed such kind of convince due to technological advancement, as it has been witnessed by the banking industry. The process has become smoother; information could be extracted in just seconds and so on. The list of advantages is immense with respect to installing the technological solutions. Automatic Teller Machines (ATM) are also exceptional aspects that have brought down huge changes into the financial services. The technology has allowed people to get cash at any point of time, no matter where they are travelling.

It increases the popularity of banking services and the genuine need of technology increases after the introduction of ATM’s. Thus, the positive impact could be realized on performance improvement, exceptional service qualities of commercial banks. The website launch is another criterion of the technological aspects. It is to acknowledge that the commercial banks need to have their website where they could come into contact with the stakeholders like customers and central bank. The expediency of launching the website is immense with respect to establishing the communication with stakeholders. Hence, the proper communication is another positive impact of IT on commercial banks. Through proper communication with central banks, the adequate amount of change could be introduced in the current working pattern. On the other hand, the change in policies or external business environment of banking industry could also be interpreted well. Overall, for commercial banks, the alignment with the stakeholders could become possible due to the technological aspects (Tansey Stephen, 2003).

The commercial banks are investing hugely on to the technological resources as it has become the base of their operations. It provides the 360-degree benefits. Service quality improvement, faster process, security, and well-established communication and so on these are some of the major advantages of investing into the technological advancements. Further, the operational cost has also maintained by the commercial banks. This positive impact is directly associated with the increment in their profitability and sustainability. Technology allows minimizing the operational cost through various ways. The objective of cost cutting could also be achieved by the banks and it most productive, the positive impact of IT on the commercial banks.

The innovation into the cash exchange, online fund transfer, and various other activities could be witnessed. The need for technological advancement is high as the industrial growth is increasing, manufacturing units are increasing, the economic growth has become the common scenario, and the per capita income of people is also increasing. Therefore, these are certain economic scenarios which put the burden on the commercial banks. Hence, to deal with these burdens there is a huge requirement of focusing on the technological solutions. It allows them to contribute to the economy in a proper way, and financial services could be promoted in a well-integrated manner. At the same juncture, it is essential to understand that the commercial banks are also categorized into various sections and types. Thus, within the commercial banks, the rise in competition is another aspect which needs the technological solutions. It is major positive impact that technology provides the market leadership position to the commercial banks. The competency increased and in result it increases the customer base as well. Therefore, the whole story is interrelated to each other; where the commercial banks can experience the positive impact of information technology with respect to acting as a link between central bank and customers (Liebowitz Jay, 1998).

2.4: Impact of Information Technology on Central Banks

The central banks are the apex bodies that can affect the whole financial structure of the country. Thus, the effectiveness of the central bank could be useful in ensuring the financial growth of the country. It is to acknowledge that information technology has provided wide opportunities for central banks to enhance their capacities so that the operations could be dealt in an appropriate way. With the help of strong IT infrastructure, the central bank can perform various functions in very smooth manner and can generate effective results. According to management experts, the productivity of the central banks could be improved at large scale. The technology is required to sustain in the global market also. Nowadays the central banks are becoming technologically advanced not only to handle the country’s financial affairs but to keep themselves updated on global affairs.

It is clear that central banks are involved in so many affairs as they need to control or to monitor the activities of commercial banks. They have to do research and construct policies, monitor the market or industry and so on. Thus, for all these activities strong IT system is required. The economic experts and banking professionals accept that the efficiency of whole banking structure and commercial banks are dependent upon the efficiency of the central bank which could simply be improved through information technology. Hence, the use and advantages of information technology could not be neglected by the central banks (Woherem, Evans, 2000). Specific positive impacts of IT on various aspects of central banks are described below:

2.4.1: IT and Data

It is essential to understand that central bank is the authority that has a connection with all the banks, and controls their activities. Thus, their technology must be effective with respect to all the dimensions of banking operations. The major aspect is that IT could enable the central bank to ensure their connectivity with commercial banks. Further, the information storage is another aspect that could be improved through proper IT infrastructure. The information technology and its firm existence within the business could allow storing or disseminating the information within the central bank. It is a very significant aspect that the central banks could extract the information easily (Keyes, Jessica, 1998).

2.4.2: Decision Making Effectiveness

At the same juncture, it is very crucial to understand that if the information storage, dissemination, and extraction are perfect, then it become possible to take the decisions in a proper way. Here, the information and data could be segregated into two categories; one which the central bank gathers from the commercial banks and other is related to the international business environment. On the basis of this information and data, the central bank makes many significant decisions. It involves designing the bank policies, loan granting policies, reverse rate, reverse repo rate and so on. With the strong IT, the keen eye on the global market could be kept. The information could be extracted in very short span of time, even after a very long period of time (Fong, Chan Onn, 1991). Thus, the central bank can compete in global markets and can ensure their strong presence along with other country's central bank.

2.4.2: Decision Making Effectiveness

At the same juncture, it is very crucial to understand that if the information storage, dissemination, and extraction are perfect, then it become possible to take the decisions in a proper way. Here, the information and data could be segregated into two categories; one which the central bank gathers from the commercial banks and other is related to the international business environment. On the basis of this information and data, the central bank makes many significant decisions. It involves designing the bank policies, loan granting policies, reverse rate, reverse repo rate and so on. With the strong IT, the keen eye on the global market could be kept. The information could be extracted in very short span of time, even after a very long period of time (Fong, Chan Onn, 1991). Thus, the central bank can compete in global markets and can ensure their strong presence along with other country's central bank.

2.4.3: IT and security

The database of the central bank is supposed to be storing many confidential details and information. Thus, it is required to build such kind of security system so that the information could keep secure forever. It must not be hacked so easily. After the digitalization of banking process, the threats of cyber attacks have been increased tremendously. Hence, the strong IT system could enable to install such kind of security system that could allow them to avoid the threats of cyber attacks. It is essential to saving the country from any kind of problems and financial turmoil (Casolaro, Luca and Gobbi, Giorgio, 2004). Hence, the central banks may experience the positive impact of information technology with respect to the strong security system as well.

2.4.4: Quickness of the Banking Operations

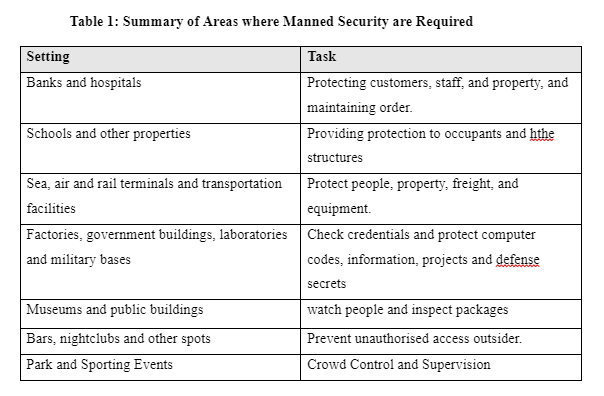

The central banks are generally involved in many operations, and heavy load could be experienced in the branches. Thus, in such situation, the central banks are required to align with the technological advancement so that the work could be handled in a proper way. The transactions of the commercial banks could be solved with swiftly. International fund transfer, connecting with other central banks or to other branches, payment, and settlement system through RTGS (real time gross settlement), improving the process of foreign exchange, could become possible through technology only. Therefore here also, the role of IT is immense for central banks (Shroff, Firdos, 2007).

These are various areas where the positive impacts of IT could be noticed. Further, various IT resources could show their expediency within the banking process of central banks. ERP system, MIS, software’s, application system, cloud computing, big data, security system like firewalls, etc. are the various sources that have the competency to put its impact on the working efficiency of central banks. The central banks could have their IT system which could be customized as per their needs and demands. Qatar bank could also avail these benefits after improving their technology system. Currently, the technological advancement level of Qatar central bank is excellent, and they use it to its competitive advantage. It allows them to represent at the global level, and the monitoring of the banking operations of commercial banks have become possible (Casolaro, Luca and Gobbi, Giorgio, 2004). Additionally with the help of strong and effective information technology the Qatar central bank can control all their financial transactions and financial affairs in painstaking manner.

2.5. Comparative Study of the Factors that Determine the Effectiveness of Information Technology in Banks

According to Bech & Hobijn (2007), there are two significant IT- related organizational factors that past studies have listed as precursors or conditions for the effective and strategic application of information technology; these include:

- Information technology planning; and

- Human capital investment and Information Technology budgeting;

2.5.1. Information technology planning

One of the most significant factors for the effective application of IT is the planning that occurs before IT implementation. For financial institutions such as Qatar Central Bank, planning is essential for ensuring the effectiveness of their IT systems. Nevertheless, as argued by Bech (2006), regardless of the huge amount of resources devoted to developing IT innovations, companies frequently overlook the importance of a tactical plan on how these innovations will be effectively applied to achieve organizational objectives. A study by Nawafleh (2015) revealed that between the years 2000 and 2001, merely 30% of organizations studied had well- defined technology implementation plans. As Nawafleh (2015) concluded, this could result in the implementation of IT systems that do not align with the organization's requirement. Therefore, this highlights the significance of tactical planning and making sure that the suitable technology is adopted to achieve organizational purposes.

Considering the case of Qatar Central Bank, with regards to the implementation of the Real Time Gross Settlement system, Qatar Central Bank had to examine the market initially and then make adequate plans prior to the implementation of the RTGS system. As previously mentioned, the volume of payments being cleared through the bank has increased greatly over a short period of time, and Qatar Central Bank was able to resolve the challenge of effectively clearing payments by planning, and implementing the RTGS system, which was a success due to effective preparation for its implementation (Bech& Hobijn, 2007). Thus, it is apparent that planning offers all organizations the time to review their current situation, and ask the correct questions; this consequently results in an effective balance and alignment between their information technology plans and their general organizational vision (Boles, 2013).

2.5.2. Human capital investment and Information Technology budgeting

This is other significant factor in the second stage of the tactical planning procedure, which is the implementation of information technology. As posted by Boles (2013), it is essential for organizations to have effective budget plans in place prior to the implementation of any technological innovation. On the other hand, Nawafleh (2015) emphasizes that it is important that organizations invest in human capital. Saigal (2008), who conducted a study on “the impact of information technology use on organizations” stated that both for-profit and non-profit organisations have two major challenges during IT implementation; these include lack of technology- trained staff and the issue of information technology experts who might not willing be to work in certain organisations. A survey conducted by Saigal (2008) revealed that less than 45% IT managers had any form of IT training. Often, staff and volunteers of the companies are ardent about the company’s vision but have minimal technological expertise and training (Kabiru et al., 2015). This poses a challenge, as Muhammad (2013) mentions, the staff of these organizations has to be well trained and knowledgeable about the new IT implementation, to ensure that these innovations are used in the most appropriate way to achieve set objectives.

Based on the above review of the literature, it can be concluded that information technology is an integral function of today’s financial institutions, as the development of various phenomena, such as ‘big data’ has made it compulsory for banks to improve upon their previous processes and procedures.

As can be seen in the case of Qatar Central Bank, the implementation of IT systems, such as the RTGS in 2002, resulted in improved efficiency of the bank’s operations, and resulted in enhanced performance and provision of services. This further buttresses the concept that IT improves the efficiency of financial institutions. Nonetheless, certain restrictions such as lack of resources, devices, skills, and training can have an undesirable effect on both workers’ and executives’ outlooks about information technology implementation, and this can consequently constrain the efficiency of an organization’s integration of IT into operations (Ishida, 2001). Therefore, to ensure that financial institutions (as well as all other organizations) fully comprehend how information technology can best improve their productivity, these institutions have to be able to use information technology for internal productivity gains, improved service delivery, and effective employee training.

As previously mentioned, regardless of the various studies on the effect of IT on commercial banks, there is barely any literature on its effect in other financial institutions such as in Central Banks. This study aims to conduct an analysis of how IT affects the activities of a Bank that does not operate with the aim of making profits and comparing the study’s findings with other for-profit organizations, to evaluate if there are any variations in the application and impact of IT in these organizations. The succeeding chapters will be focused on achieving this objective.

Chapter 3 - Research Methodology

3.1: Introduction

The research methods and methodologies are important foundations for any significant investigation. They guide the research effort to answer the research question. This chapter will describe research process, research design, sample collection, sources of information and so on.

3.2: Research Process

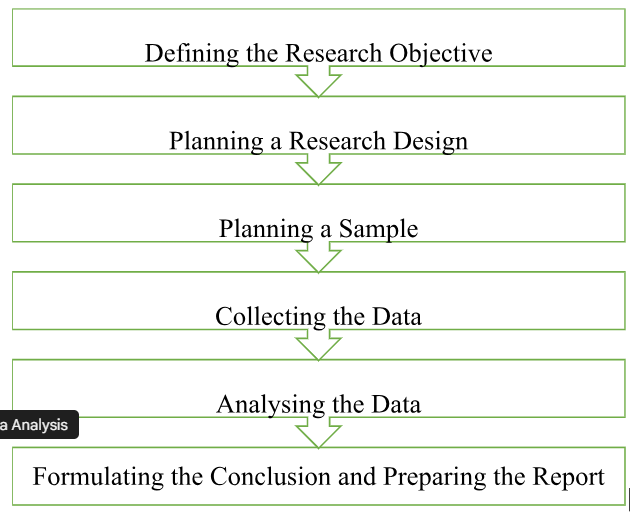

The Scientific investigation involves a systematic process that requires being objective and collecting information for analysis so that the researcher can come to a good conclusion. This process is used in all research, irrespective of the research method that is being followed. In this research paper, the following activities have been followed as presented in figure 3.1 and as Babinet al indicated (60).

Figure 1: The Systematic Research Process

(Source: Zikmund, William, 1997)

3.3: Research Methods

The research methodologies chosen to study the efficiency gained through Information Technology (IT) in Central Bank, and Qatar Central Bank is used as an example for the study, the method of the research is mixed as it will use both qualitative and quantitative analysis. An online survey in the form of a questionnaire sent to specific employees in QCB.

3.4: Case Study Research Method and Sampling

Case studies provide several ways of deriving information regarding a particular case/unit/organization under study. They are useful because they are one of the most flexible of research designs. They allow the researcher to retain the holistic characteristics of real life events while at the same time investigate empirical events. Shell et al. (1992) define a case study as an investigation of a contemporary phenomenon within its real-life context, when the boundaries between the phenomenon and context are not clear, and in which multiple sources of evidence are used.

In this research, the Qatar C Bank was chosen as the entity for the case study. The limitations are that what holds true for the Qatar Central Bank may not necessarily hold true for all similar organizations. However, using information obtained from secondary research it would be possible for the research to make observations which provide insight into the empirical questions of the research. Creswell (2013) explains that generalizations in case studies can take place when the same study is repeated in new case settings. In the current research since we only examine one case, we stay away from making generalizations as far as possible, and we only make generalizations where the current case supports the existing body of knowledge. Anomalies are therefore noted with the appropriate degree of particularity.

One of the methods used for data collection in this research in order to understand the phenomenon is the questionnaire survey. It was formulated to consider key concepts, essential to deriving finer results. Lack of appropriate design can lead the questionnaire to be used in a particular survey to generate inaccurate or meaningless results (Baxter et al. 100) and hence the questionnaire was designed in consideration of the various factors that could impact its usefulness to the research. This will be discussed in the following sections.

Sampling (Bryman and Bell 186) is a simple process of building a representative sample of a wider group/population, whose characteristics ought to be studied for a defined purpose. These small proportions of people are considered to represent the entire/overall population such that what is true for this small sample can generally be held to be true of the entire population. The respondents have to be chosen in a way that allows them to relate entirely to the questionnaire developed by the researcher (Baxter et al. 98). In this research, a case study had been performed with the employees of ‘Qatar Central Bank’ (QCB) as subjects. A small number of the employees of the organization are used to build the sample for this study. The primary research aimed to gain more information on the influence of IT on QCB’s organizational performance, productivity and efficiency.

3.5: Research Questions/Objectives

Research Questions have a huge impact on this research process since they are the forces that remind the researcher, ‘the people concerned, the purpose and objectives of the study and the issues dealt with the study’ (Bryman and Bell 712). Most importantly, they assist in giving precise attention to the core subject of the study and thereby extract appropriate answers for the same. The research questions/objectives framed for the current research are as follows:

- To understand the relationship between IT and performance improvement in Qatar central bank.

- To assess the impact of IT on decision-making effectiveness

- To identify the role of IT in creating the business process quicker and accurate

- To recommend various ways to improve performance and efficiency through information technology.

3.6: Data Collection through Survey Questionnaire

‘Data Collection’ is crucial to all research. Two of the more common methods of data collection are questionnaires and interviews (Baxter et al. 253). Interviews help to yield rich data but are time-consuming and can reach only a small number of respondents. Questionnaires, on the other hand, are useful for collecting quantitative data from a larger number of respondents. In order to obtain a representative sample, it is necessary to obtain a relatively larger sample than can be obtained by interviews in the current research, given the fact that it is an academic piece of research. Furthermore, it was evaluated that it is research questions can be adequately answered by the collection of data using a questionnaire. Hence, the current research employs an online survey questionnaire that aims to gather responses from employees about their association with QCB, their dependency on IT, level of IT usage, etc.

Questionnaire – Key Concepts, Response Receiving Mode & Online Platform Used:

Questionnaire – Key Concepts, Response Receiving Mode & Online Platform Used: Some of the key concepts (Bryman and Bell 265) considered while framing this questionnaire survey are as follows:

- Design and format of the questionnaire cannot be lengthy or difficult to read/understand

- The researcher should understand the types of questions required to obtain the data or information needed from the respondents(for better understanding),

- Researchers should be able to define the number of closed (multiple choice answers available for respondents are limited, for, e.g., yes/no) and open (qualitative choice of answers are available) questions to be included in the questionnaire

- Questionnaire type, e.g., straight questions, rating-scale questions,

- Constantly examine if the questionnaire is efficient at retrieving consistent results

- Mode of receiving survey responses, e.g., Email, Personal Interview, Online Webpage.

The Survey used in this research was disseminated using a number of methods such as email, dissemination through social media, etc. The research questions in this survey have been formulated in order to achieve the research objectives. Except for the ‘1’ personal (factual) attribute question regarding their functional level in QCB and two other questions requiring respondents to fill in without any restrictions, the rest follow a ‘Likert’ rating scale format. In this format, a five-point scale is used to indicate response strength.

The following questions were formulated:

- Please specify your staff status – To evaluate the impact of the IT systems by staff groups if any.

- When did you join the Central Bank? Please indicate which Central Bank also – This was to evaluate the impact of resistance to change if any.

- In a typical day, how often do you use computer systems / applications? – To understand user behavior.

- How would you rate your ability to retrieve data from past records? – To understand user skill levels

- Please rate your agreement with this statement: Your existing IT systems meet all business requirements – To understand user acceptance of the IT systems

The remaining questions aim to gather information about user opinions of various aspects of the system, in terms of what is good and bad about the system. The qualitative answers solicited are expected to shed light on aspects that have not been anticipated in the questionnaire; the multiple choice questions help those who want to be brief but also help to jog the thoughts of the users who could contribute greater insight.

- Your existing Information Technology systems reduce the need for manpower in Central Bank

- Your information technology systems help to increase accuracy in tasks

- Your existing Information technology systems help in anticipating customer needs (Customer could mean other departments)>

- Your information technology systems help you in planning and decision-making

- Your existing information technology helps to facilitate the automation of business processes

- Your existing information technology systems help you do more

- Your existing information technology systems help you do FASTER. There is room for improvement in the Information Technology systems that are currently used in the organization

- The new Information Technology systems introduced have improved my productivity

- The new Information Technology systems introduced have improved the productivity of employees in general

3.6.1: Rationale behind the Choice of Questions in the Questionnaire

Certain questions, focal to this survey had been framed with a significant degree of reasoning. In order to get a better knowledge about the background of the respondents taking up this survey, their status within the hierarchy of their organization was determined (Survey Question 1). Instead of classifying the working population on their respective designations, they have been segregated in accordance with their functionalities. This helps the research to group the respondents into functional groups with varying levels of IT usage.

It is important to understand that employees are not only individuals but also have their roles within the organization. Therefore, a the research requires a better insight into the role and extent of IT usage associated with the employees’ respective job specifications, how efficiently they are able to satisfy their roles with the use of IT, how they can make better use of IT to improve their productivity and thus ease the efforts made in performing business operations. In order to analyze the employees based on this perspective, respondents had been asked if their IT systems met all their business requirements(Survey Question 5).In the banking sector, IT products are basically IT applications that render ‘banking services’ to both people supporting the data/information needs of staff responsible for (banking) operations and customers (Swierczek 271). The efficiency of these services decides the bank’s productivity. In view of this fact, the respondents were queried about the impact of IT on reducing the manpower required at QCB (Survey Question 6).

3.7: Questionnaire Administration and Data Analysis

The questionnaires were distributed to all the employees in the QCB. This amounted to X employees, of which Y responded, resulting in an overall response rate of Z%. Statistical data analysis using SPSS will be used to extract relevant information from the survey results. Other than this the thematic analysis will be used to analyze the subjective information.

3.8: Research Philosophy

The relevance of research philosophy is immense with respect to understanding the viewpoint of researcher towards the subject matter. The researcher has the leverage to gather the data or information through various dimensions. The different perspectives could be investigated in order to understand the subject matter. There are mainly two kinds of research philosophies that could be practiced by the researcher; it includes the interpretive research philosophy and positivism research philosophy. In interpretive research philosophy, the researcher has more advantage and freedom to explore the subject matter from different angles. It reads the truth from various dimensions. On the contrary, the positivism research philosophy deals with the universal facts and figures which remained unchanged and same under all the circumstances. It is to acknowledge that the interpretive research philosophy is more suitable when the researcher is dedicated to focusing on the exploration of content. Here in the current scenario, the interpretive research philosophy has been put into practice by the researcher. It is something that can enable a researcher to understand the role of IT in Qatar Central Bank. The viewpoints of employees and staff people could be understandable from different aspects and variety of opinions could be included in the study.

3.9: Research Approach

Here the researcher is aiming at understanding that how the study could be conducted. Moreover, the researcher can focus on conducting the study. There are two kinds of approaches; inductive and deductive research approach. In inductive research approach, the researcher first identifies the statement and observes it in various instances and then reaches out at the conclusion. Here the whole study is based on the experience or the observation. On the contrary, the deductive approach is the one in which the researcher test the validity of the particular statement. Observation is all about to check the feasibility and reality about a particular situation. Thus, both inductive and deductive approaches are differing to each another at large scale. In the current report, the researcher is assessing the situation of IT within the central bank. The expediencies of IT could be investigated properly with the help of inductive approach. The huge level of observations could be done and with the help of scenario analysis, the researcher can definitely concentrate on gaining desired results out of the study. Overall the inductive research approach is favorable for the current study.

3.10: Ethical considerations

The major ethical issue that has gained huge consideration into the current report that during the survey the identity of the respondents has been kept unrevealed and secret. It is one of the major ethical issues that have gained priority by the researcher. Other than this the researcher has focused on the fact that the results must not be altered under any circumstances. The originality and authentic results have been provided in the report. Moreover, the element of plagiarism has also taken care of by the researcher. In the current report, none of the matter is steeled from any other sources. Whole information is genuine and completely plagiarism free.

Chapter 4 - Data Analysis and Interpretation

4.1: Introduction

The utility of Information technology towards improving organizational efficiency, specifically to the Central Banks such as QCB, considering their role in carving the financial path of a nation was understood from the literature review. Following the research methodology, a questionnaire was designed, and the responses were collected from the respondents through an online survey. A detailed analysis of the collected data is conducted in the ensuing sections, so as to understand the associations between the variables and draw valuable findings.

4.2: Profile of Respondents

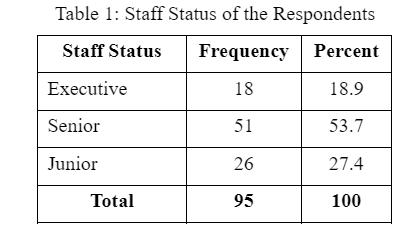

A total of 95 respondents were considered for the study. As can be observed from Table 1, 18 of them are Executives (18.9 percent), 51 percent are seniors (53.7 percent), and the rest are juniors (27.4 percent). Thus, more than half of the respondents are seniors, considering their position on the organizational ladder.

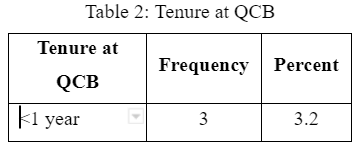

From Table 2 below, it can be gathered that majority of them (54.7 percent) have been working with QCB for more than six years. The sample includes about 28 percent of employees who were with the Bank for 4 to 6 years. The rest have an experience of fewer than four years the respondents (13 percent were working with QCB for 1 to 3 years and 3 percent for less than one year). Thus, most of the employees are well-versed with the work, processes and procedures of the Bank.

Table 3: Respondents by Department

Considering the various departments at QCB, the sample belonged to almost all the divisions, as illustrated in Table 3. This ensured that the sample would be representative. About 17 percent of them were from Banking, Payments and Settlements section; 11 percent are from Supervision and Control Department; 10 from Investment and nine each from Legal Affairs and Financial Stability Planning and Relevant statistics.

4.3: Usage of Information Technology in Various Divisions

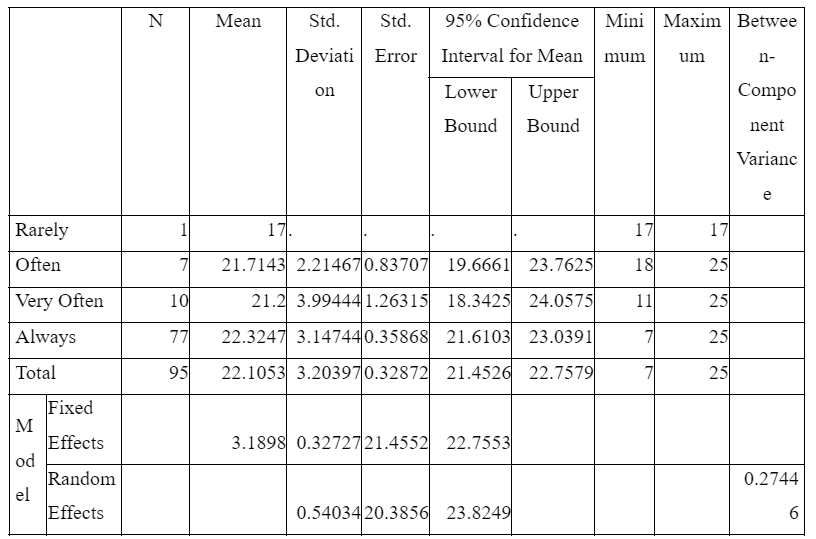

4.3.1: Frequency of Usage Daily

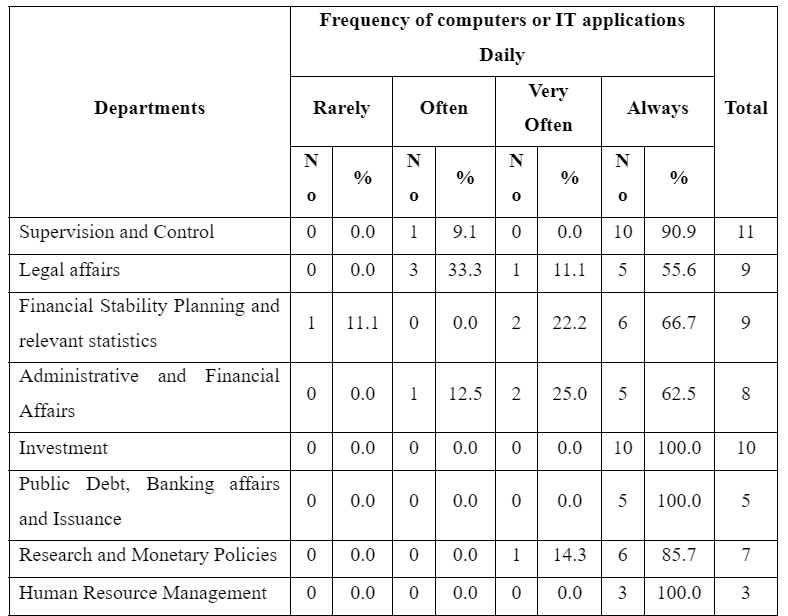

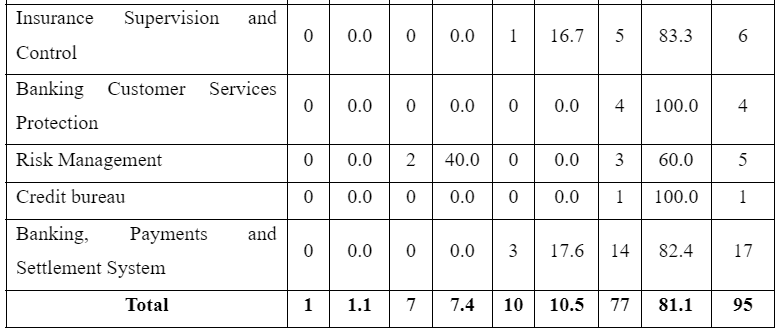

Table 4: Frequency of Usage of IT on Daily Basis by Departments

The respondents were questioned regarding their frequency of computers and IT usage daily, and none of them said that these applications are not used at QCB. The results are presented in Table 4. Thus, it can be inferred that IT is certainly part and parcel of each of the departments of the Central Bank. Considering the other responses of the sample, 91.6 percent agreed to wide and more frequent usage (response of ‘very often’ and ‘always’ put together). High percentages in this regard can be observed in the case of Investment, Public Debt, Banking Affairs and Issuance, HRM and Customer Services Protection divisions.

A total of only 8.5 percent of the respondents feels that the IT and applications are used less often on a daily basis, who mainly belong to Risk Management and Legal Affairs, as was the case with the extent of IT usage in decision making. Therefore, it appears that these are the departments where the work is influenced by other factors, which do not permit the usage of IT to a large extent.

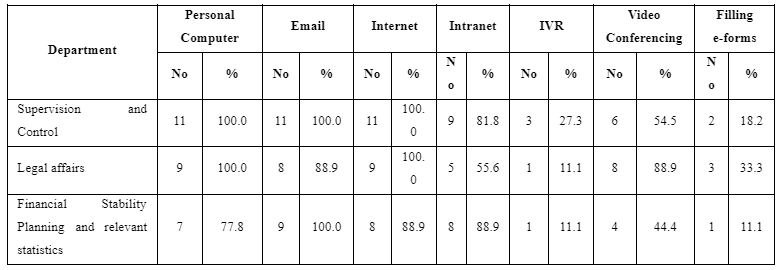

4.3.2: Usage of Tools of Office-Automation

When the usage of tools of office automation among the respondents was observed, it was found that those from all the departments use Personal Computers, be it laptop or a desktop (except few from Financial Stability and Banking, Payment and Settlement System), email (except few from Legal Affairs Division) and internet (except some of the employees from Financial Stability Planning, Risk Management and Banking, Payment and Settlement Systems). The other facilities of automation such as Intranet, IVR, Video conferencing and ease with filing e-forms are used to a lesser extent by almost all the divisions, except Credit Bureau. Some of the respondents also confided to the usage of dedicated tools such as Core Banking Systems and general software such as MS Office. One of the respondents from Banking, Payments and Settlements Division also revealed that QCB heavily relies on technology. Thus, all the tools of office automation seemed to be used by most of the divisions, though with varying extents, as described by the employees.

Table 5: Various Tools of Office-Automation by Department

4.3.3: Usage of MIS in Business Process Systems

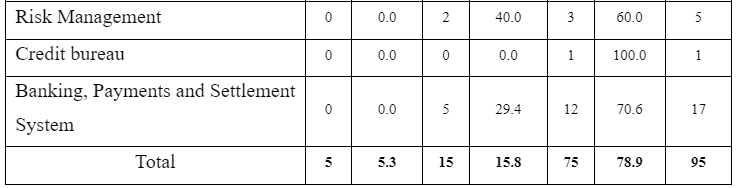

Table 6 depicts the responses of the sample to the question on the frequency of usage of MIS in business process systems. Widespread use of the MIS has been confessed by 78.9 percent of the respondents while 15.8 percent feel that it is averagely used, and the rest say that it is rarely used. Extensive use is found by the employees belonging to Research and Monetary Policy and Banking and Customer Services Protection divisions. The sample belonging to Department of Financial Stability Planning seemed to make limited use of MIS in business processes and those of Legal Affairs and Banking, Payments and Settlement Systems use it passably.

Table 6: Frequency of Usage of MIS in Business Process Systems by Departments

4.3.4: Usage in Decision Making

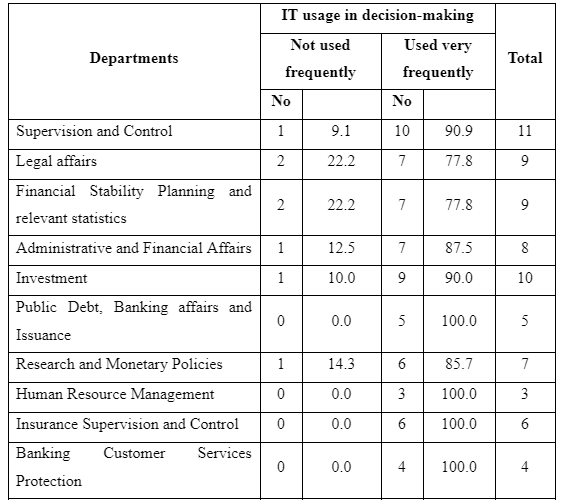

When the sample were questioned on the extent of usage of IT in their department towards decision-making, with five options ranging from ‘Never’ to ‘Always’, more than 87 percent of them responded with either ‘Very often’ or ‘Always’, leaving a total of just 12 respondents in the three other categories. Therefore, the responses were re-grouped into two categories, ‘Not used frequently’ and ‘Used very frequently’. The relevant data is presented in Table 7.

Table 7: Extent of IT Usage in Decision Making by Departments

It can be observed from the table that IT is extensively used in almost all the departments, as more than 75 percent of the respondents from each of the divisions, except those from Risk Management (60 percent only) accepted the fact. However, there is a sizeable chunk of respondents in some of the departments (2 respondents each) who think that the IT is not used frequently in decision making, who belong mainly to Legal Affairs, Financial Stability Planning, Risk Management, and Banking and Settlements. These variations in the level of usage of IT might be attributed to the impact of externalities and contingencies relevant to the Government Directives and fluctuations in the financial and other factors that might necessitate due consideration at the time decision making.

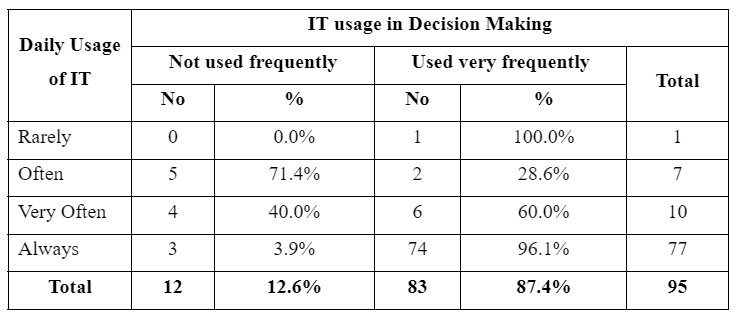

Table 8: Extent of Usage of IT daily by Its Use in Decision Making

The general usage of IT on a daily basis among the respondents is cross-tabulated with its usage in decision making. About 96 percent of the instances where IT applications were frequently used on a daily basis, it is used for decision making also. However, in cases where it is used very often every day, only 60 percent of the times are IT being used for decision making. IT is used for decision making in only 28 percent of the situations in which it is used often for general purposes. An independent sample t-test is run using SPSS to understand the association between extent of usage of IT on a daily basis and its utility in decision making. Table 9 shows the results of the test.

Levene’s test for equality of variances helps determine which of the t-statistics are to be used. It can be observed that the p-value corresponding to test statistic F, which is shown as a sig. for the Levene Test (0.002) is less than the set confidence level of 0.05, in the case of IT usage daily. Therefore, the results from the ‘equal variances not assumed’ row are to be read. The sig. (two-tailed) value is 0.001, which is less than this confidence level. This depicts that the usage of IT towards decision making differs significantly based on the daily usage of IT and computer applications by the respondents.

Table 9: Independent Sample t-Test Results

On the whole, computers and IT are being used by all the divisions of QCB. Therefore, the sub-hypothesis one from the research methodology is accepted, which states that Information technology is used in all divisions at QCB. Further, the analysis in this section also proved that the IT applications are used very frequently towards decision making in most of the departments. Therefore, the sub-hypothesis two from the research methodology stands accepted. It states that the Information technology is significantly used as a tool for decision-making at QCB. However, such usage is contingent on the general utility of IT in the job and work of the employees on a daily basis.

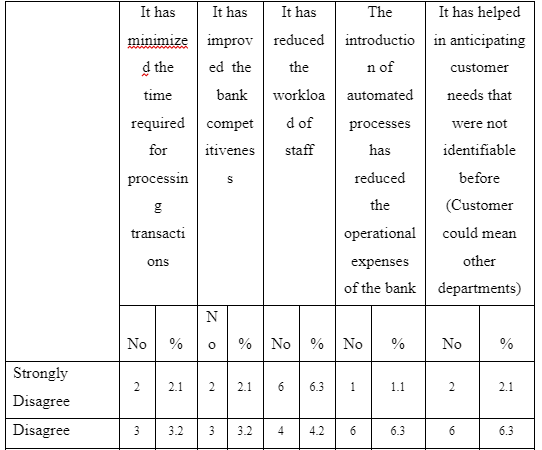

4.4: Improvements in Operational Processes in QCB due to IT

- It has minimized the time required for processing transactions

- It has improved the bank competitiveness

- It has reduced the workload of staff

- The introduction of automated processes has reduced the operational expenses of the bank

- It has helped in anticipating customer needs that were not identifiable before (Customer could mean other departments)

Table 10: Agreement to Statements on Improvements in Operational Process Due to IT

The frequencies of degrees of agreement to these statements by the respondents are tabulated and presented in Table 10. It can be observed that more than 85 percent of the sample either agree or strongly agree to each of these improvements. However, about 5% to 10% of the sample disagree or strongly disagree to the improvements in each operational process due to the usage of IT.

The total score for the level of agreement to the improvements in the overall operational processes at QCB was calculated by summing up the agreement scores of individual items on a 5-point scale. This total improvement in operational processes agreement score is plotted against the extent of usage of IT on a daily basis, using the One-way Analysis of Variance (ANOVA) in SPSS. This test is used because one of the variables is qualitative and the other is quantitative, and the qualitative variable has more than two possible values (5 in this case).

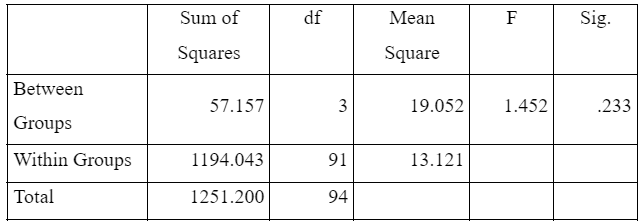

Table 11: Descriptive Table

The descriptive table gives the various groups of the independent categorical variable, which is the extent of usage of IT on a daily basis. The means and standard deviations are also given in the table 11. The next one is the ANOVA table, which is shown in Table 12. It gives the associations within and between the groups at confidence level 0.05. The p-value for the test statistic F, shown by sig. is 0.233 is more than the confidence level. This illustrates that the improvements in operational processes do not differ significantly with the level of usage of IT on a daily basis, as stated by the respondents.

Table 12: ANOVA Table

From the above analysis, it can be inferred that the improvements brought about by IT in the operational processes at QCB are felt and agreed by 85% to 93% of the respondents. Therefore, the sub-hypothesis three from the research methodology, which states that Information technology has significantly improved operational processes at QCB through automation, is approved. However, this agreement to improvement is not statistically related to the level of usage of IT on a daily basis by the respondents.

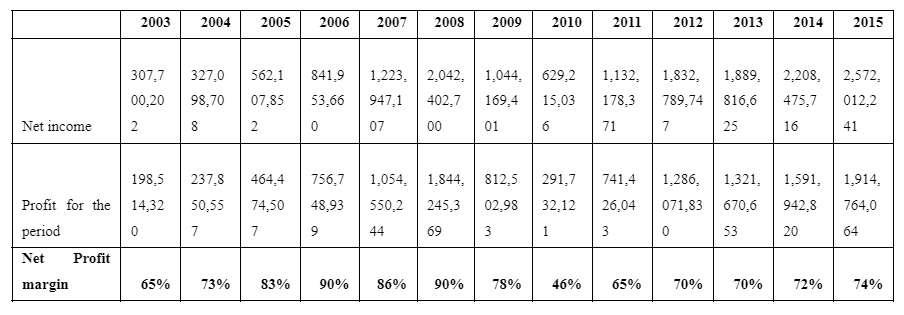

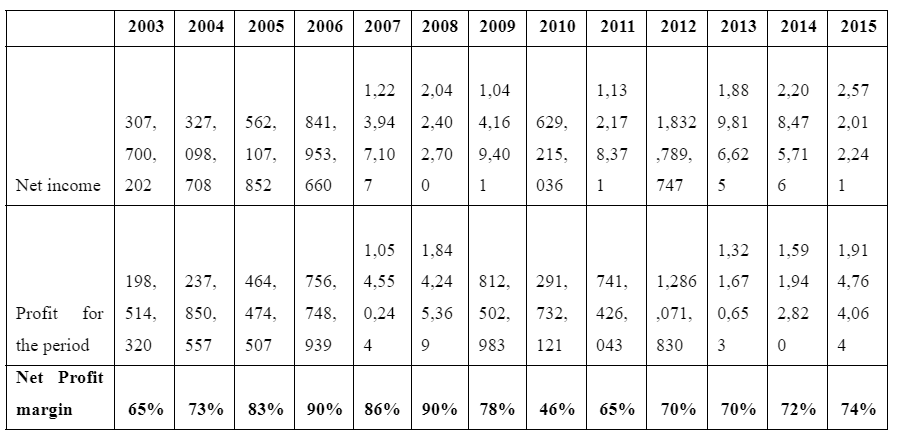

The results above were further collaborated through the analysis of the profit margin since the major introduction of Automation in 2003. The results below show growth in the profit margin until 2010 where a sharp decline occurred. Afterward, a sustained increase was also observed. One of the reasons for the growth in the profit margin may be due to a reduction of operational expenses compared to revenues due to more efficient processes following automation. Thus, the observed responses in the questionnaire largely collaborate.

Table 13: Income Statement

Source: QCB Income Statement

4.5: Improvements in Human Capital at QCB due to IT

Questions regarding the level of agreement of the respondents to statements related to the improvements in human capital that were observed at QCB, after the use of Information Technology. The following aspects are used to measure the improvement in human capital:

- The number of personnel necessary to do a job has decreased

- It has improved the performance of employees

- It has promoted better supervision by supervisors/managers

- It has increased the focus on employee development

- It has reduced the bureaucratic distance that exists between the various levels of organization

Table 14: Agreement to Statements on Improvements in Human Capital

The frequencies of degrees of agreement on the intended improvements in human capital as felt by the sample are illustrated in Table 14. More than 85 percent of the respondents agreed or strongly agreed with most of these statements. For the question related to the improved focus on employee development after the onset of IT initiatives, the sample showed a little lesser agreement at 80 percent, with almost 15 percent expressing a neutral level of agreement to this and 5 percent disagreed with it. Thus, it seemed that the computer-based applications are yet to be streamlined to address this point among the HR management tasks. The disagreement to the other statements was found to fall in the similar range as that for the improvements in work processes. About 5% to 10% of the sample disagreed or strongly disagreed to the human capital improvements through the usage of IT.

The agreement scores of individual statements related to improvements in human capital on a 5-point scale are added up to obtain the human capital improvement score at QCB. Then, one way ANOVA is conducted by considering the total human capital improvement score as the dependent variable and the extent of usage of IT on a daily basis as the independent variable.

Table 15: Descriptive Table

The descriptive table gives the various groups of the independent categorical variable, which belong the extent of usage of IT on a daily basis. The means and standard deviations for the total human capital score for every change in the value of the independent variable are presented in the table 15. The ANOVA table (Table 16) depicts the associations within and between the groups, to bring forward the differences in dependent variable with corresponding changes in the independent variable. The confidence level set is 0.05. The p-value for the test statistic F, shown by sig. is 0.33 is more than the confidence level, which proves that the improvements in human capital caused due to IT did not differ significantly with the level of usage of IT on a daily basis.

Table 16: ANOVA Table

This evaluation led to the conclusion that improvements in human capital because of the IT initiatives at QCB were observed and felt by 80% to 90% of the sample who were employees from its various departments, with different levels of experience and belonged to the different rungs of the organizational ladder. Therefore, the sub-hypothesis four from the research methodology, which states that Information technology has significantly improved human capital management at QCB through automation, stands true. However, this agreement to improvement is not statistically related to the level of usage of IT on a daily basis by the respondents.

4.6: Reduction of Operational Expenses at QCB due to IT

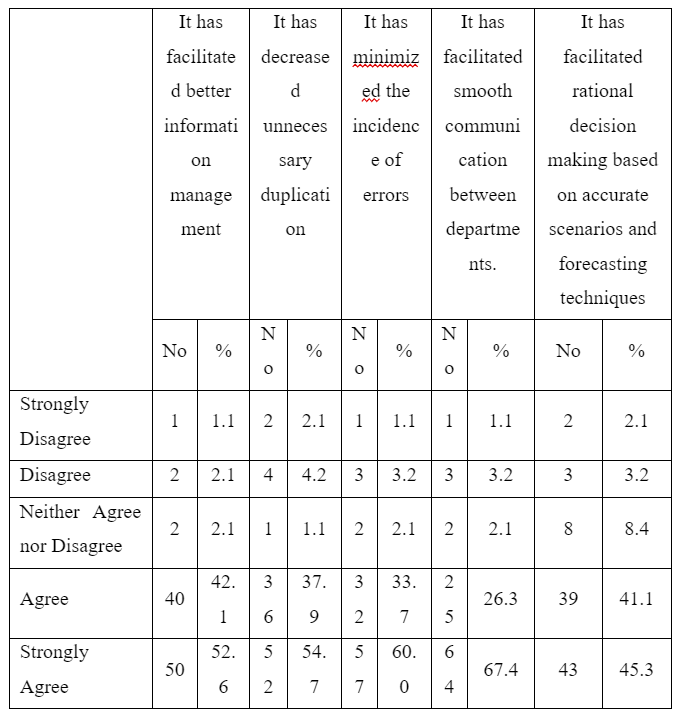

The questionnaire also sought to understand how much would the employees of QCB included in the sample agree with the statements relevant to a reduction in operational expenses after the organization started using IT in its various divisions and activities. The following considerations were utilized to measure this aspect:

- It has facilitated better information management

- It has decreased unnecessary duplication

- It has minimized the incidence of errors

- It has facilitated smooth communication between departments.

- It has facilitated rational decision making based on accurate scenarios and forecasting techniques

Table 17: Agreement with Statements on Reduction in Operational Expenses

The frequencies of degrees of agreement with the statements related to the observed decrease in the operational costs by the sample are shown in Table 17. Almost 86% to 94% of the samples were in agreement with all the statements in this regard. About 5% to 6% of the sample disagreed or strongly disagreed to the reduction in operational costs due to the usage of IT.

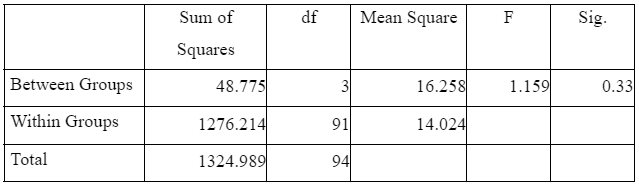

The agreement scores of individual statements related to a reduction in operational expenses, which were measured on a 5-point scale, are summed to calculate the total reduction in operational expenses score at QCB. Taking this total score as the dependent variable and the level of IT usage every day as the independent variable, one way ANOVA is conducted using SPSS.

Table 18: Descriptive Table

Descriptive table gives the various groups of the independent categorical variable, which belong the extent of usage of IT on a daily basis. The means and standard deviations for the total reduction in operational costs score for every change in the value of the independent variable are presented in the table 18. The ANOVA table (Table 19) depicts the associations within and between the groups, to bring forward the differences in dependent variable with corresponding changes in the independent variable. The confidence level set is 0.05. The p-value for the test statistic F, shown by sig. is 0.286 is more than the confidence level, which proves that the reduction in operational expenses caused due to IT, as felt by the sample, did not differ significantly with the level of usage of IT on a daily basis.

Table 19: ANOVA Table

The exploration has thus directed towards the assessment that the decrease in operational expenses due to the usage of IT at QCB, was felt by 86% to 94% of the sample. Thus, the sub-hypothesis 5 of the methodology is accepted. It proposed that the Information technology has significantly reduced the operational expenses at QCB. However, the level of observed reduction in this aspect is not statistically associated with the level of usage of IT on a daily basis by the respondents.

4.7: Adequacy of IT initiatives at QCB

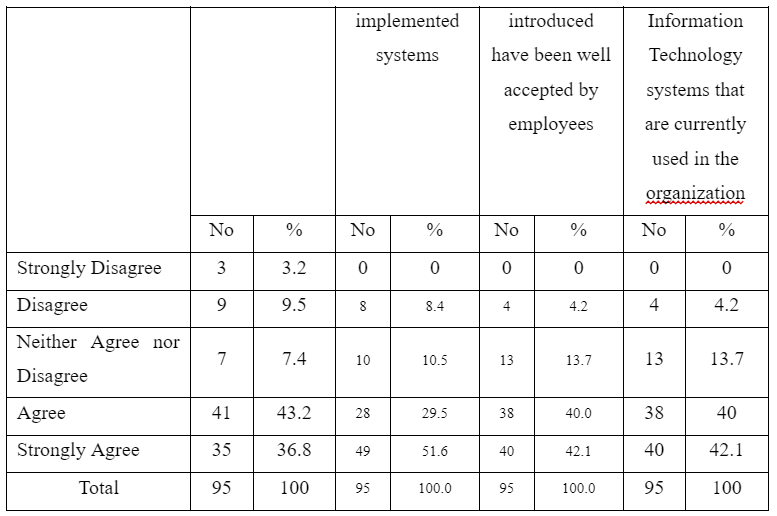

The respondents were provided with four statements related to the adequacy of the IT usage at QCB. These are as follows:

- The existing IT systems meets all business requirements

- Employees are able to properly utilize the implemented systems

- The new Information Technology systems introduced have been well accepted by employees

- There is room for improvement in the Information Technology systems that are currently used in the organization

The level of agreement to each of these statements is provided on a five-point scale ranging from ‘strongly disagree’ to ‘strongly agree’. The frequencies of the responses are tabulated and presented in Table 20.

Table 20: Adequacy of IT initiatives at QCB – Frequency Table

About 80 percent of the respondents felt that the IT systems existing at present at QCB are adequate, and they are well-accepted and being utilized properly by the employees. However, the same percentage of the sample (80 percent) also felt the need for improvement in the present IT system. About 80 percent of the respondents felt that the IT systems existing at present at QCB are adequate, and they are well-accepted and being utilized properly by the employees. However, the same percentage of the sample (80 percent) also felt the need for improvement in the present IT system.

When probed further regarding the nature and areas of improvement necessary in the IT usage and application aspects, the responses of the sample varied as the question was open-ended. The following points were suggested by the respondents:

- Improvement in Core banking, Settlement systems, payment gateways, procurement system, query system, reporting system, access to central server, data management, decision support system, HR management, data and document security, vendor management, authorization, and money transfer systems,

- Customizing the systems to incorporate the needs of each division, after thorough discussion with the relevant personnel

- Bringing out mobile applications relevant to the operations of the Bank

- Automation to the level of self-service for various processes at the Bank

- Publishing user manuals in the local languages for the software and updates

- Updating systems with the upcoming demands and trends

- Unified database management system

- Need for a single sign-in system

- Need for an internal social hub

- Speech-enabled input system

Table 21: Results of the Profit Margin Analysis from 2003 to 2015

CHAPTER 5: CONCLUSIONS AND RECOMMENDATIONS

Having conducted a detailed analysis of the data collected, in the previous chapter; this section draws conclusions from the findings. It also discusses them while considering the backdrop of the points presented by the various authors in the literature review. Finally, it envisages making certain recommendations that would be helpful to QCB and other such Central Banks in understanding the worth of Information Technology in delivering organizational efficiency.

The sample selected for the study is representative in terms of including employees from different levels on the organizational ladder, their years of working at QCB and various divisions of the firm. Thus, this provides huge scope for the responses of these employees and the results drawn out from these responses, to reflect the opinions of most of the staff members of QCB in general.

IT Usage

IT, computers and related applications are frequently used in most of the divisions of QCB, as agreed upon by 87 percent of the respondents. In the legal affairs and risk management divisions, these are used to a lesser extent. Coming to the tools of office automation, Personal Computers, email and the internet are the most common ones, utilized by more than 95 percent of the respondents, belonging to various divisions. However, others such as Intranet and video conferencing are not usually employed, especially by the Legal Affairs division again. IVR is only used by half of the respondents.

More or less, every department at QCB is using information technology. This goes along the point put forward by Aliyu and Tasmin (2012); IT is here to stay, even in the case of non-profit organizations, to support their functioning and organizational processes. The necessity of such IT initiatives in non-profit organizations was also emphasized by Hackler and Saxton (2007) and Nawafleh (2015) and the findings of the study support the authors.

The differences in usage of IT among the various departments might be attributed to the skill level, the necessity of one-to-one interactions, the requirement of social and financial awareness and the situational adaptability requirements of the jobs within the departments. The payments and settlement systems, legal affairs, customer services protection, financial stability planning aspects are vulnerable in one or more of these regards and thus, require human involvement and judgment to tackle some of the issues rather than just follow the scenarios played out by the heartless software or hardware.

Efficiency in Operational Processes and Reduction in Expenses

The statements related to improvement in the operational processes of QCB due to IT were presented to the sample to respond to their rate of agreement between them. More than 83 percent of the respondents agreed that it has minimized the processing time, reduced workload, reduced operational expenses and helped in understanding consumer needs better. Thus, the operational processes are perceived to be going on the path of improvement with the usage of IT, by the employees. It is surprising to note that this perception of improvement is not dependent on the extent of general and routine usage of IT by them.

At the same time, the employees also agreed that the information technology has been facilitating better information management, reducing the costs of duplication and manual errors, it has further been contributing to smooth communication and rational decision making. These points have been agreed by more than 85 percent of the employees included in the sample. This finding backs the remarks of Tansey (2003) that IT has improved the calculation power.

Operations management is about increasing the efficiency of work which would lend to handle efficiently the needs of the consumers. Considering this, information technology has been helpful in minimizing resource requirements such as personnel, time, and money; along with giving the Bank a competitive advantage by better assessment of the needs of consumers and drawing out scenarios based on real-time information. It has also improved communication and decision-making processes. Thus, the results that would lead to organizational efficiency are being perceived by the employees, though they seem to be oblivious of these long-term impacts of the elements of their jobs that are automated. This explains the reason for the above scenario revealed by the present study. Efficient integration of IT into the operations of an organization was found to improve its efficiency by Boles (2013), and this study proves the point.

As remarked by Blackbaud and Campbell (2012) in Central Banks, QCB has also based its IT initiatives on three reasons, which are analyzed and proved by this study. These reasons are: reduction of costs, meeting the customer needs better and improvement in information management.

Efficiency in HR Processes