Strategic Cost Management

- 11 Pages

- Published On: 11-12-2023

Introduction

The strategic analysis helps an organization to study the internal and external environment in which the business operates. This supports the strategy formulation process and assists in identifying the factors that impact an organization and its decision-making process. In the current period, there has been a significant increase in competition among the different organizations. This, in turn, has raised the need for applying suitable strategic tools that would help the company in managing the business efficiently and reducing the cost as well. In this regard, this particular essay focuses on critically analyzing two different strategic tools that are used by organizations for implementing their strategy and evaluating how the tools can be used for managing and reducing cost, providing valuable insights for business dissertation help.

Discussion- Critical Evaluation of the Strategic Tools

The Balanced ScorecardThe strategy an organization adopts and the activities it performs are interlinked, and these together derive its strengths in business. The performance of the organization deteriorates if this link is overlooked. According to the report of Harvard Business Review (2020), the performance of an organization is measurable. However, in this regard, it has been further argued that often the managers ignore performance measurement as part of organizational strategy. In this context, Caudle (2008) has highlighted that every organization should consider size as an essential part of the management process. The concept of a Balanced Scorecard was first introduced by Norton and Kaplan in the year 1992, which is a framework comprising of different factors that measure the performance of the organization. According to Varasi (n.d.), The Balanced Scorecard was earlier used as only a performance improvement tool, and now it is one of the efficient strategies implementing a tool that mainly focuses on measurement.

A Balanced Scorecard is used by different organizations worldwide for managing strategies. This enables bridging a connection between planning and management and developing a relationship between the project and people working on it, and successfully tracking the success (Balanced Scorecard Institute, 2020). According to the report of Harvard Business Review (2020), the different perspectives of Balanced Scorecard are financial, customers/Stakeholders, internal process, and organizational capacity.

The financial perspective of the Balanced Scorecard is one of the vital factors as it assists in measuring the financial performance of the company. Financial performance is the critical indicator of success in the long-run period. The different measures used to measure financial performance are return on investment, number of debtors and creditors, profitability, and cash flow, among others (Caudle, 2008). Caudle (2008) highlights that the financial perspective is suitable for measuring the short-run financial performance of the organization. Edwards (2006) stated that one of the vital issues with the economic outlook is that it is wholly based on the past data, and thus it does not measure the current performance instead focuses on the past. Therefore, it has been argued that the financial perspective does not support analyzing the future performance of the company. According to Effiong & Beredugo (2015), in this global world, competition is increasing, and perpetual changes have been evident in the case of customer demand and expectations of the shareholders. Thus, it becomes vital for companies to implement efficient cost management strategies. In today’s world, historical information used in Balanced Scorecard is not adequate for the managers to take the cost management decisions effectively. However, Caudle (2008) stated that performance measurement using the financial perspective is one of the vital components of cost management.

Another component of the Balanced Scorecard is the customer perspective that directly influences customers. This includes various factors such as the company's response towards customer complaints, customer survey response, and several customers, among others (Edwards, 2006). In this competitive world, the success of an organization depends on customers significantly. Thus, the company should ensure customer satisfaction and retention for long-term growth. It has been further argued that more dissatisfied customers are likely to shift their interest towards the other suppliers for fulfilling their requirements (Harvard Business Review, 2020). In the business world, retaining customers is very important to remain competitive in the marketplace. Analyzing customer’s perspectives enables finding loyal customers. Besides, the loyal customers are likely to have in the long run and reduce the cost to the company as they attract more new customers for the company and helps in maintaining stable profit (Chapman, 2012)

Caudle (2008) stated that the internal business perspective of the Balanced Scorecard is about evaluating the business process that would help in fulfilling the needs of the customers and shareholders. This factor measures different business processes such as production time, re-order cost, and processing time. According to the report of Balanced Scorecard Institute (2020), evaluating the internal business process allows the company to measure how well the business is functioning. Also, it enables the company to determine whether its products and services are meeting the requirement of the customers or not. Edwards (2006) stated that analyzing the business perspective is also useful in managing cost. It focuses on the internal operation and can be improved to reduce expenditure based on its performance.

The learning and growth perspective of the Balanced Scorecard is about evaluating the development/learning ability of the company. It measures the power of an organization to implement change and improve performance to achieve organizational goals. Also, this perspective counts the infrastructural needs of the company that is vital to achieving this perspective goal. Apart from these, this particular perspective also helps in measuring the ability of the company to implement innovation in business, for instance, design in the launch of a new product (Edwards, 2006). Caudle (2008) highlighted that for learning and growth perspective, people are considered the most excellent resource. Norton and Kaplan, through this Balanced Scorecard framework, have tried to explain that learning and knowledge are more valuable as it not only contributes to individual development but also supports corporate development.

From the above critical evaluation, it has been evident that a Balanced Scorecard is a combination of different financial and non-financial factors that has a mutual relation and ultimately result in better financial returns for the organizations. This relationship can be better understood from the vertical vector relationship figure given below.

Figure 1: Vertical Vector Relationship

Source: (Edwards, 2006)

Kaizen

Kaizen is another strategic tool that can be used to minimize cost by concentrating on eradicating non-value adding functions. Kaizen is a Japanese term that means ‘change for better. Kaizen is based on the philosophical thought that everything can be developed. This indicates nothing is status quo, and there is a constant effort to grow, which leads to small, frequent indiscernible changes through time. Kaizen works to enhance two aspects, procedures and outcomes. The developments in these two areas lead to a minimization of waste, comprising minimization of costs. Wastes in organizational processes can frequently result in considerable expenditure for the corporate facility; therefore, even small developments can influence overall expenses (Olszewska, 2019). Although Kaizen’s main objective is not nearly a reduction in costs, it can be an excellent result. Another method that Kaizen can assist with organizational costs is by the implementation. Small incremental variations, which are at the core of Kaizen tend to be inexpensive and straightforward to implement. The developments made through this tool may not lead to direct cost-saving, but they can perform to make procedures operate smoother or to make work setting better for employees. In the end, these small changes build up to more significant developments in the organization and more considerable savings in cost (Jayakumar, 2015).

According to Bungau & et al. (2014), the critical objective of Kaizen philosophy comprises cost minimization and production growth by the eradication of losses. There are two functions in Kaizen philosophy, one is activities that generate added value, and the other one is activities that do not cause added value. The elimination of losses yields the growth of value-generating functions in the total flux of activities. Any tasks that intend to increase the value-creating process will enhance the working situations and hence increase the cost-saving. Okoye & et al. (2013) stated that one of the methods that consider continuous development based on small changes is a method based on Kaizen philosophy. Kaizen encompasses the function of the company as a whole; nevertheless, it is possible to utilize it only in the chosen fields or workplaces. Concerning the organizational objectives, one of Kaizen’s most vital applications is Kaizen costing. It is the use of the Kaizen concept in the field of cost management. Considering management decisions based on this method permits organizations to optimize their functions and opens up additional prospects, which they did not have access to initially owing to high expenses and too much inflexibility in the role. Utilizing Kaizen's philosophy in cost is specifically efficient when it is escorted by the procedure of conscious development of sales budget. The combination of possibilities provided by budgeting procedure and values of Kaizen costing generates a strategic tool empowering the evaluation of several cost decisions and the choice of the most ideal option for the organizational unit in a given period.

The norm behind Kaizen costing use is on accomplishing small, gradual, but constant developments in the production procedure at minimal expenses. Ellram (2000) observed that Kaizen costing certifies product fulfills or surpass customers’ demand for quality, functionality, and prices to sustain the product’s competitiveness. According to Rof (2012), cost-saving can be accomplished by sequential elimination of every procedure that would enhance the product’s manufacturing cost without corresponding growth in value. He recognized certain features as certifying the effectiveness of Kaizen costing. For example, Kaizen does not strive for perfection; instead, it seeks gradual development in the present situation at an excellent expense. It permits managers to implement choice in the application of their knowledge and personal abilities. Kaizen inspires cooperative decision-making, i.e., the thoughts of many are better than the idea of a single individual.

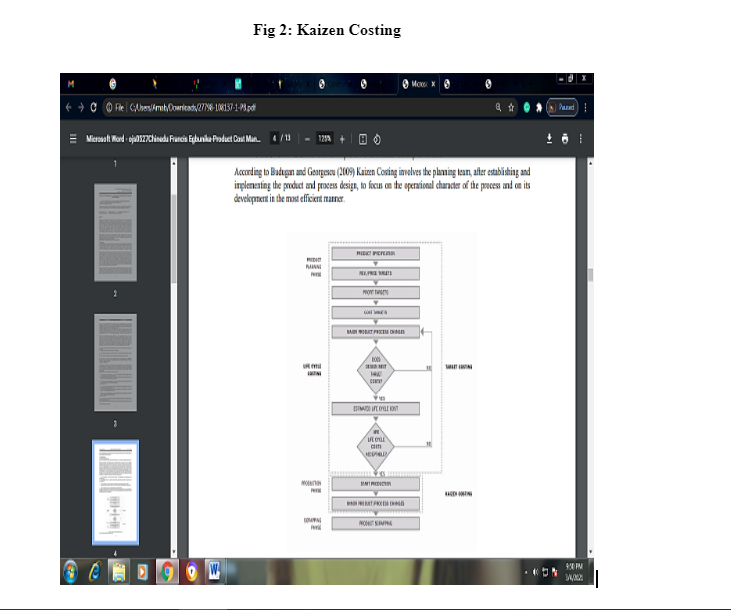

According to Budugan & Georgescu (2009), Kaizen costing comprises the planning team, after establishing and applying the product and procedure design, to concentrate on the functional feature of the procedure and on its growth in the most effective way.

Take a deeper dive into Strategic Cost Management with our additional resources.

Continue your exploration of STRATEGIC MANAGEMENT OF BURTON RETAILS with our related content.

Conclusion

These two strategic tools, the balanced scorecard and Kaizen, are available to organizations to manage and to reduce the expenses in the business. A balanced scorecard helps to understand and to evaluate the business procedures from different perspectives, like financial perspective, customer perspective, inner business perspective, and learning & growth perspective. By understanding performance from different perspectives, a balanced scorecard gives a picture of the opportunity for improvement, which is one of the key elements for cost management in any organization. Then again, the Kaizen tool help organizations for continuous improvement through the eradication of wastes. Kaizen costing method is used to discard all the activities that cannot add value and implement activities that add value, generating changes in the organization. Such changes result in cost savings indirectly in the organization.

Dig deeper into Strategic change management with our selection of articles.

References

Balanced Scorecard Institute, 2020. Balanced Scorecard Basics. [Online] Available at: https://balancedscorecard.org/bsc-basics-overview/ [Accessed on 04 March 2021].

Bungau, C. & et. Al., 2014. Kaizen Implementation for Cost Reduction in Manufacturing Process Product "Driver Control Board”. 3rd International Conference on Quality and Innovation in Engineering and Management, pp. 1-12.

Budugan, D. & Georgescu, I., 2009. Cost reduction by using budgeting via the Kaizen method. Scientific Annals of the “Alexandru Ioan Cuza” University of Iasi-Economic Sciences, Vol. 56, pp. 3–9.

Chapman, J., 2012. The Importance of Customer Retention — An Empirical Study. [Online] Available at: https://www.toptal.com/finance/venture-capital-consultants/the-importance-of-customer-retention-an-empirical-study [Accessed on 04 March 2021].

Edwards, S., 2006. Balanced Scorecard. [Online] Available at: https://www.cimaglobal.com/Documents/ImportedDocuments/cid_image_balance-scorecard_june06.pdf.pdf [Accessed on 04 March 2021].

Ellram, L. M., 2000. Purchasing and supply chain management’s participation in the target costing process. Journal of Supply Chain Management, Vol. 36, pp. 39–51.

Effiong, S. & Beredugo, S., 2015. Strategic Cost Management: Recipes for Productivity Rating of Nigerian Manufacturing Company. Open Journal of Finance, pp. 1-8.

Harvard Business Review, 2020. Putting the Balanced Scorecard to Work. [Online] Available at: https://hbr.org/1993/09/putting-the-balanced-scorecard-to-work [Accessed on 04 March 2021].

Jayakumar, K., 2015. Kaizen Costing – A Management Technique. International Journal of Business and Management Invention, Vol. 4, No. 9, pp. 1-5.

Okoye, P. V. C. & et. Al., 2013. Product Cost Management via the Kaizen Costing System: Perception of Accountants. Journal of Management and Sustainability, Vol. 3, No. 4, pp. 114-125.

Olszewska, K., 2019. Cost management with budgeting and Kaizen Costing. World Scientific News: An International Scientific Journal, Vol. 133, pp. 171-190.

Rof, M. L., 2012. Kaizen Costing Method and Its Role in the Management of an Entity. The Young Economists Journal, pp. 104–109. Varasi, R.., n.d. Balanced Scorecard as a strategy formulation tool. [Online] Available at: https://varasi.com/strategy/balanced-scorecards/ [Accessed on 04 March 2021].

- 24/7 Customer Support

- 100% Customer Satisfaction

- No Privacy Violation

- Quick Services

- Subject Experts